Isa 6:9-12 And He said, Go, and tell this people, You hear indeed, but do not understand; and seeing you see, but do not know.

Make the heart of this people fat, and make their ears heavy, and shut their eyes; lest they see with their eyes, and hear with their ears, and understand with their hearts, and turn back, and be healed.

Then I said, Lord, how long? And He answered, Until the cities are wasted without inhabitant, and the houses without man, and the land laid waste, a desolation, and until Jehovah has moved men far away, and the desolation in the midst of the land is great.

Newsletter 5862-012 The 3rd Year of the 5th Sabbatical Cycle The 32nd year of the 120th Jubilee Cycle The 28th day of the 3rd month, 5862 years after the creation of Adam The 5th Sabbatical Cycle after the 119th Jubilee Cycle The Sabbatical Cycle of the Tithes to the Widows and Orphans

May 16, 2026

Shabbat Shalom to the Royal Family of Yehovah,

I want to start off with the following short announcement. If you are interested in joining us for Sukkot in Tennessee for 2026, we have a limited number of spaces left. You need to drop me an email with how many there are in your family that are joining us. Once they are gone, then they’re gone. There are a number of activities to do in the area, along with restaurants if you want to go out.

Have you considered your plans for Sukkot this year? Sightedmoon will be gathering in East Tennessee and we have room for a few more families. Please reach out to us at admin@Sightedmoon.com if you would like more information. One group is staying in an RV/camping site and another group will be staying in a cabin.

Attention Sightedmoon & Mishpacha Fellowship

All praise to Yehovah! By His hand, our team is busy planning Sukkot 2026 for you. This Year’s Theme: “PUT ON THE ARMOR OF GOD” The Place: Sevierville, TN When: August 28 th thru September 06 Cost for Lodging: $ 550 to 600 Plus cost for Meals: $ 300 All this and more for ten days, Armor of God the PLAY, Auction Table, Bible Jeopardy, Teachings, and a Wedding. Space is limited, so secure your place with a deposit of $ 250 USD, today. Balance is due by July 31 st 2026.

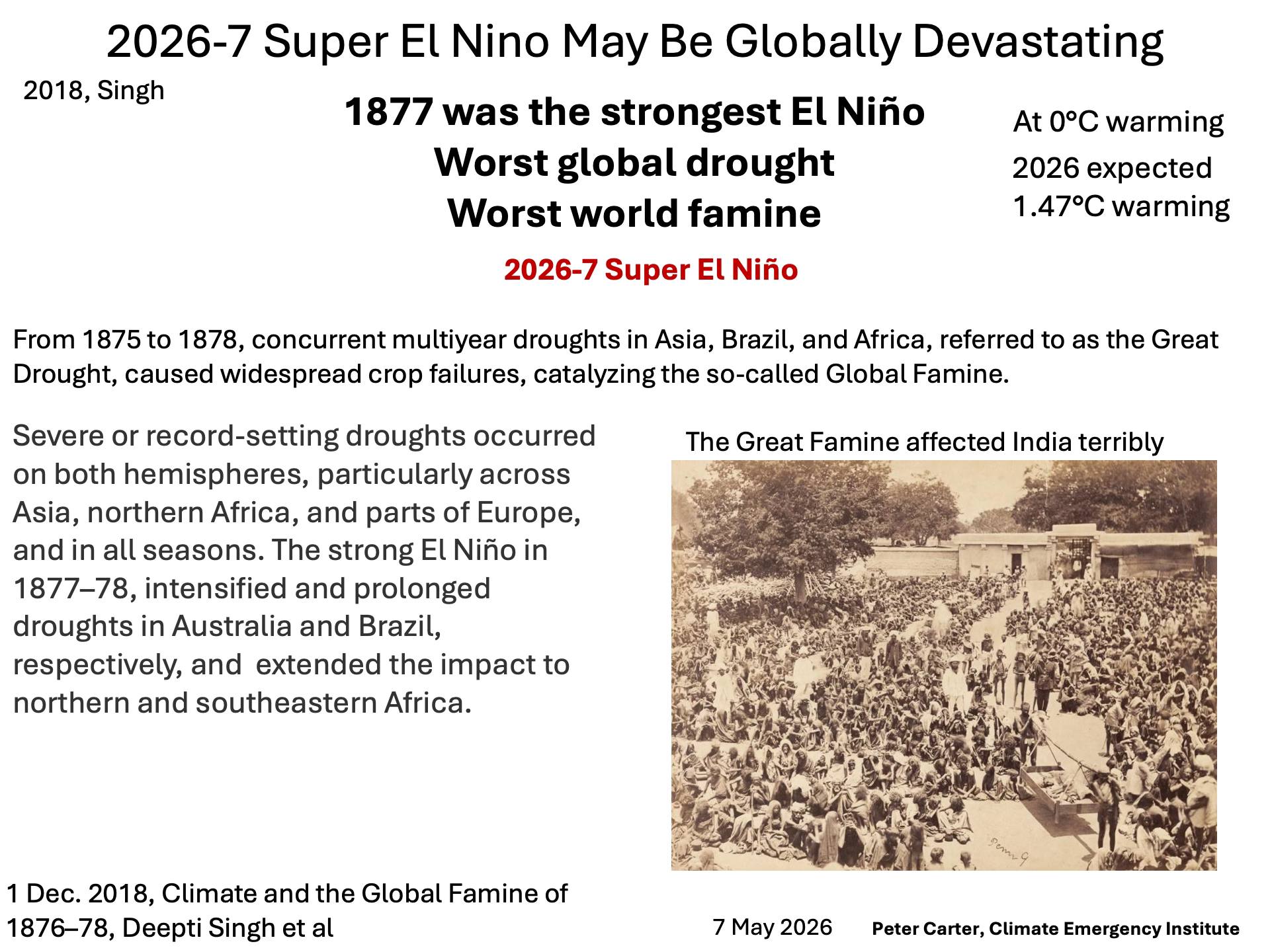

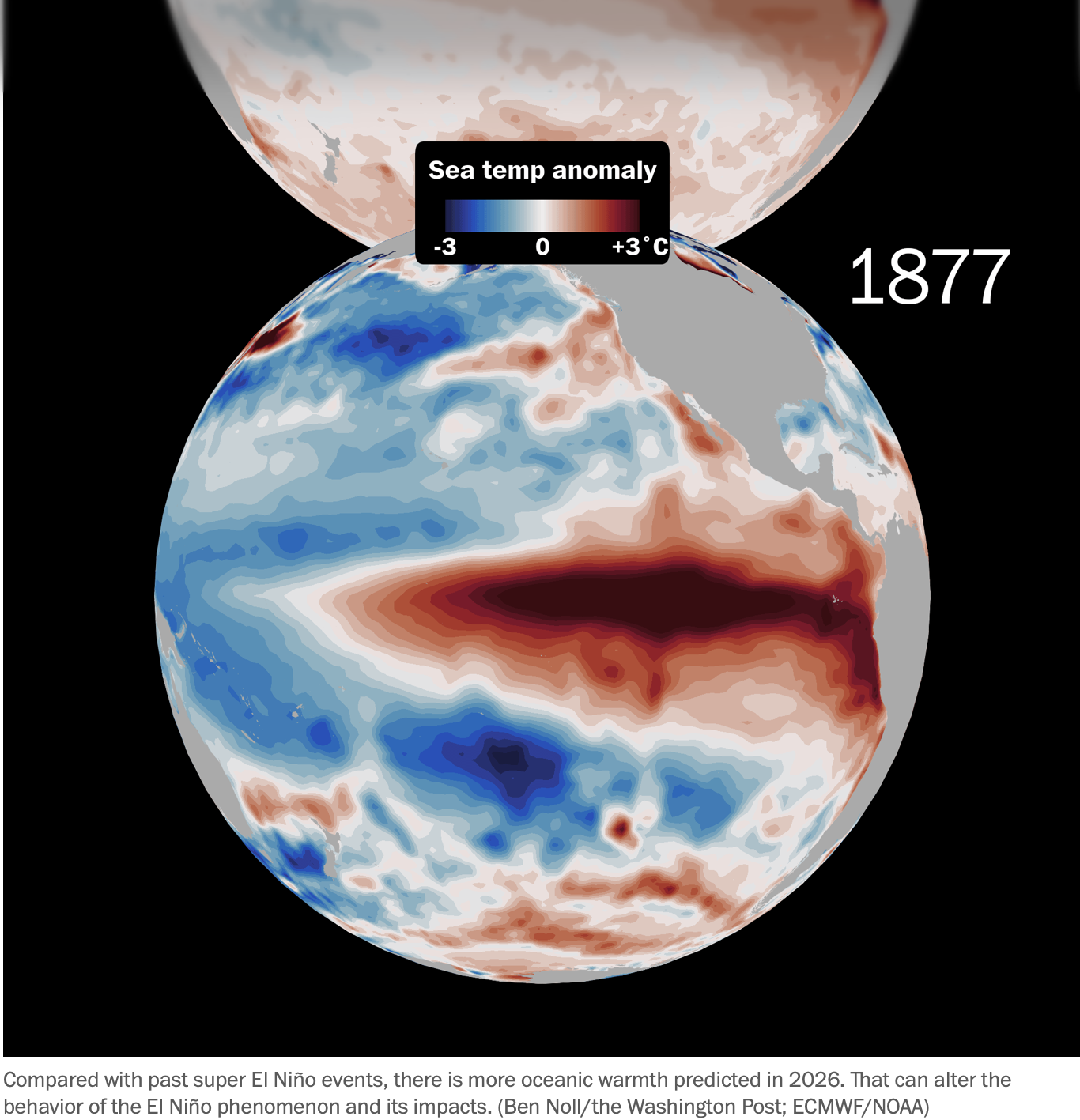

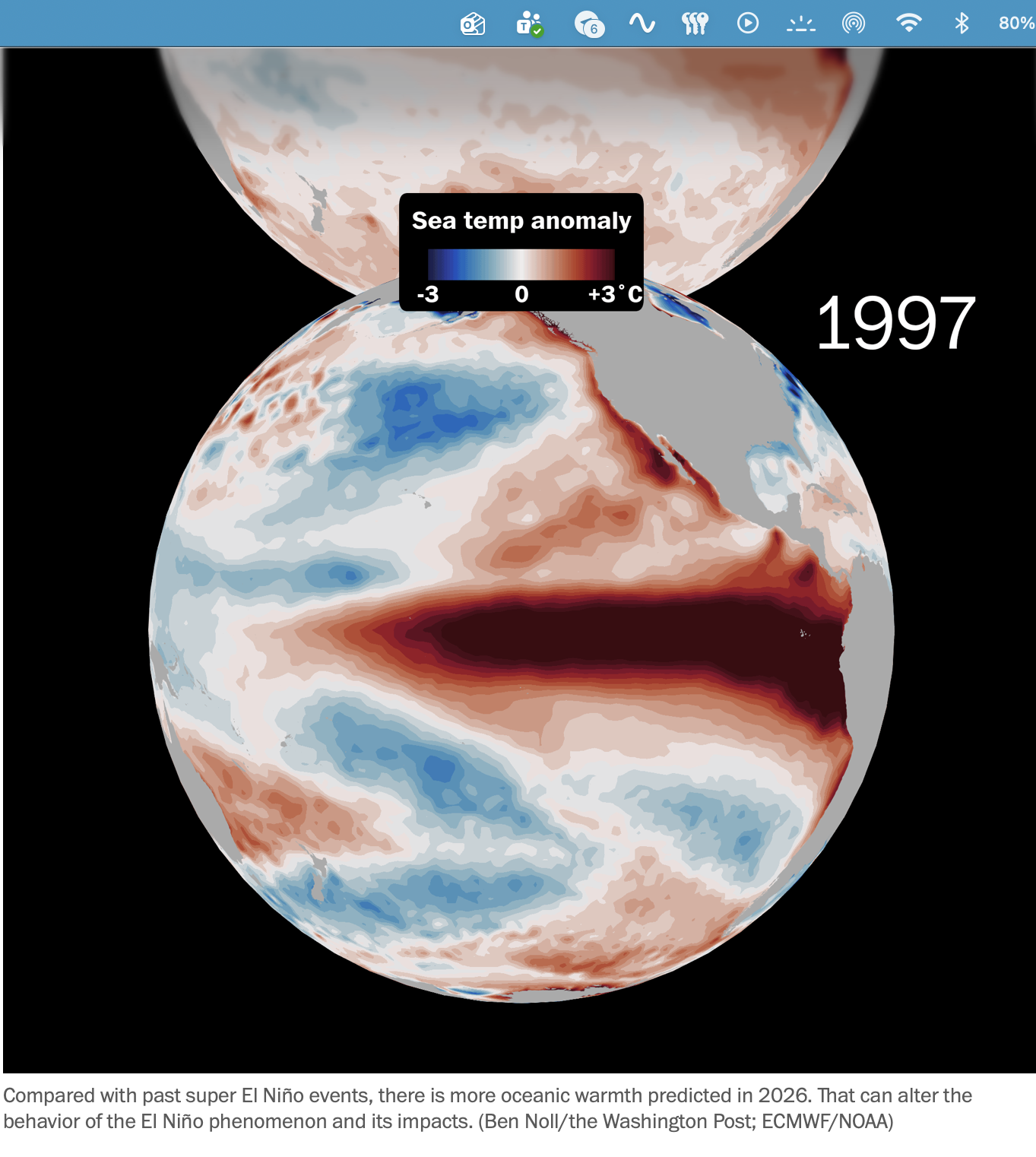

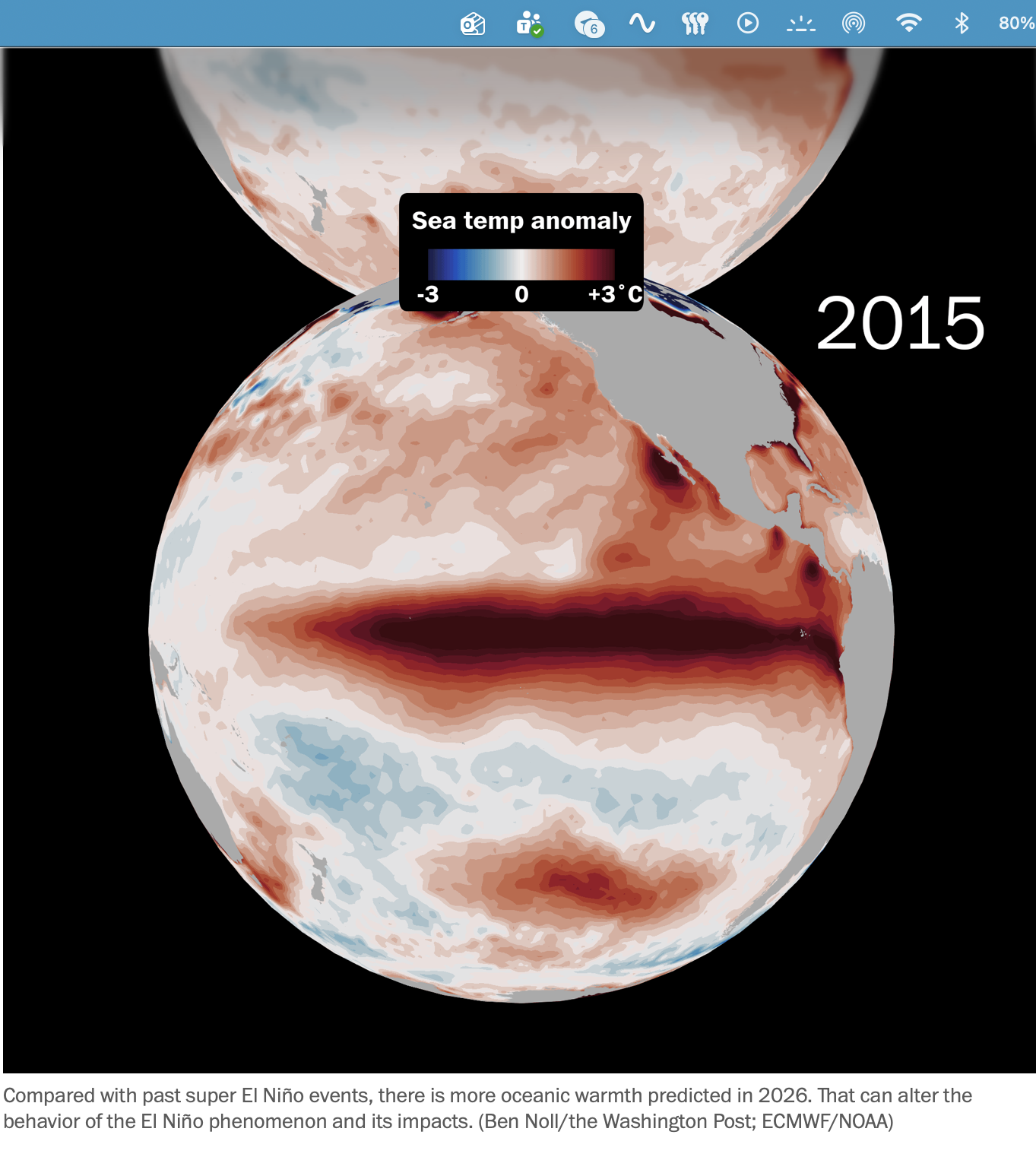

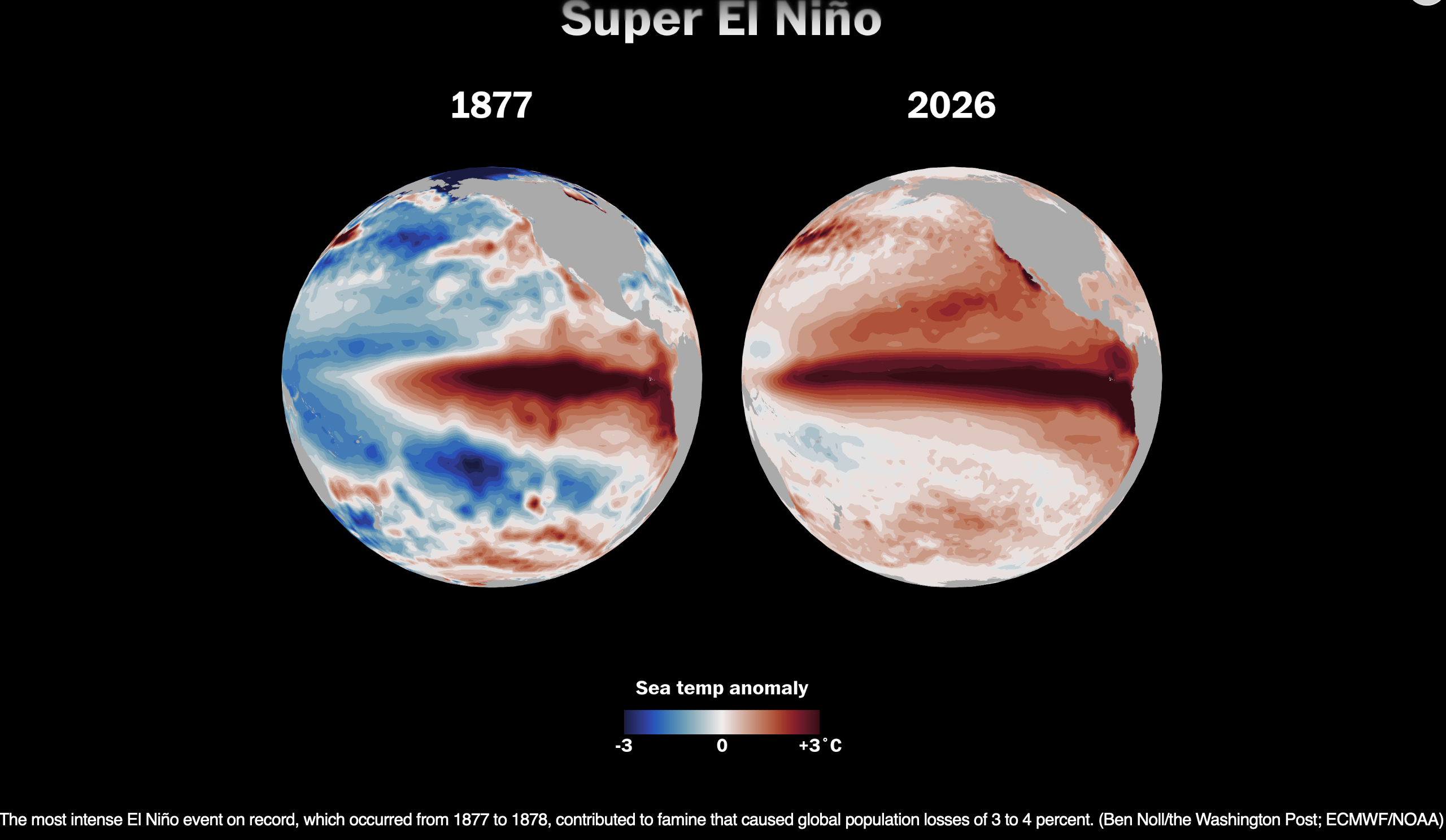

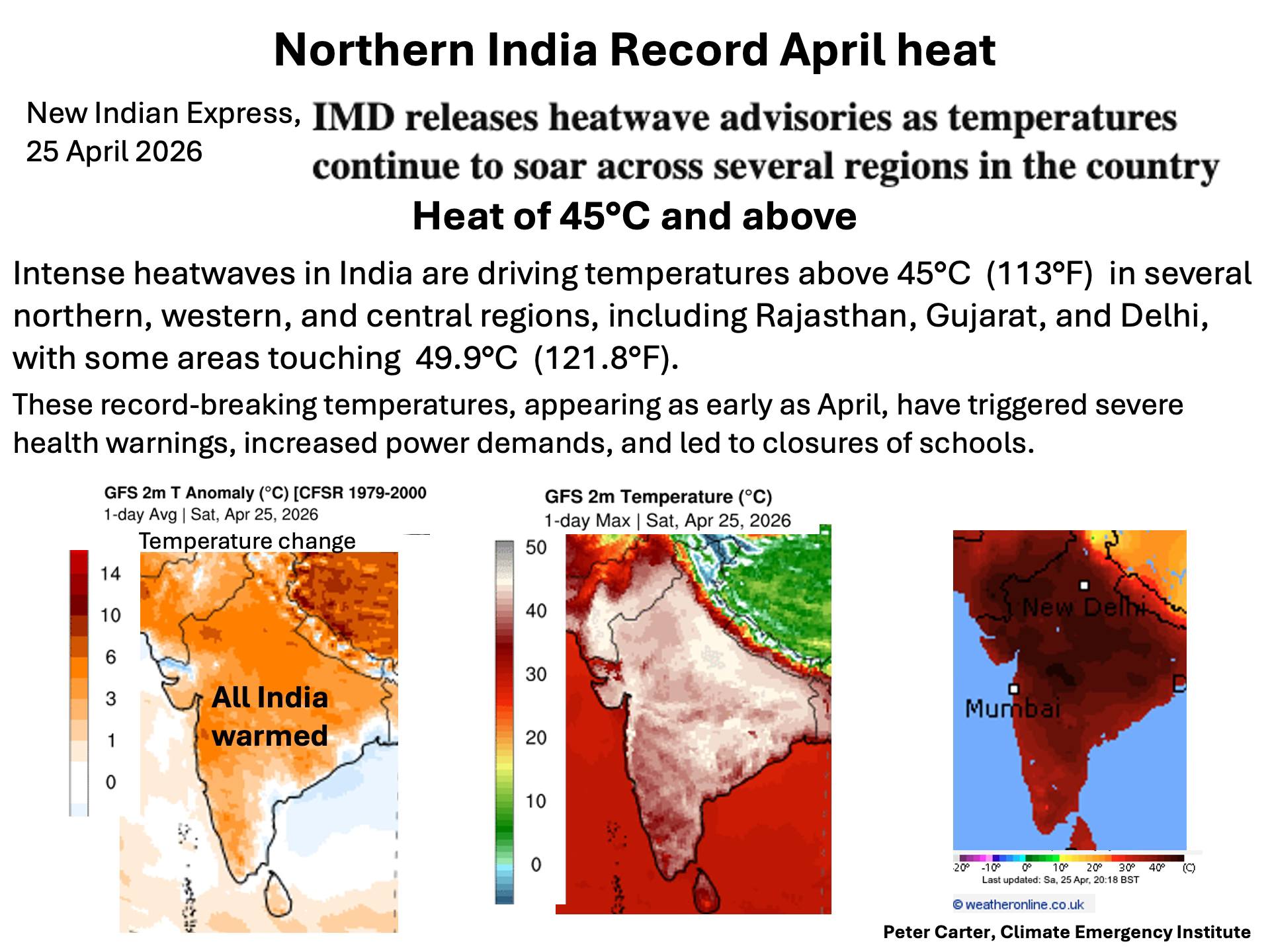

This week we are talking about the coming famine from the El Niño point of view. It is making the news, and in every single report I see, they blame it on the oil companies and the burning of fossil fuel. Some of them even mention the report that we are also mentioning about 1877 and how that El Niño caused hundreds of millions to die around the world. They did not have cars then

Notice the automobile went from a rare luxury item to a common sight on North American roads remarkably quickly. Notice the years when this took place.

The pivotal moment came in 1908, when Henry Ford introduced the Model T. In 1913, he perfected the moving assembly line at his Highland Park factory in Michigan. This revolutionized manufacturing: cars went from being hand-built, expensive toys for the wealthy to mass-produced vehicles that ordinary people could afford. The price of a Model T dropped dramatically — from around $850 in 1908 to under $300 by the mid-1920s.

By the mid-to-late 1920s, cars had truly become commonplace across the United States and Canada. In 1920 there were about 8 million registered vehicles. By 1929 that number had exploded to roughly 23–26 million. For the first time in history, America had approximately one car for every 5 people. Paved roads expanded rapidly, gas stations and garages sprang up everywhere, and the car culture (suburbs, road trips, drive-ins, and personal freedom) began to reshape society.

By the 1930s, even through the Great Depression, automobile ownership was considered normal for middle-class families. The car had transitioned from a novelty to an essential part of daily life. But there were no cars in 1877.

What this is telling me is that the El Niño of 1877 was not caused by Global Warming or Climate Change. You can’t blame that on men burning fossil fuels. Sorry. It just does not fit. But if you look at your Sabbatical and Jubilee charts, the 1877 famine came in the 5th Sabbatical cycle, which is, according to Lev 26, the cycle of famine. And once again this El Niño is lining up to be one of the worst ever super El Niños on record. So it is not Global Warming, stupid; it is not Climate Change stupid. It is Yehovah, the God of creation, who told us in Leviticus 26 what would happen and the order it would happen in IF we did not obey the commandments in Leviticus 23 and 25.

People want to blame these world catastrophes on other men or men in back rooms or the Jews. Make no mistake, these things are coming precisely because of men NOT OBEYING YEHOVAH. PERIOD!!! And it is Yehovah who is sending them. Not HAARPE, Not Chem Trails, and not fossil fuels. YEHOVAH and He alone, is sending them on this rebellious world. We have watched the temperatures rise from the start of the Jubilee cycle in 1996, and this year is going to top them all. At the same time, the two witnesses come to stop the rain. So give credit to Yehovah, and once you do, then more people will possibly begin to repent. But if it is the oil companies’ fault, then no one needs to repent. See the difference?

Join Our Sabbath Meetings

Join Our Sabbath Meetings

There are many people in need of fellowship and who are sitting at home on the Sabbath with no one to talk to or debate with. I want to encourage all of you to join us on Shabbat, and to invite others to come and join us as well. If the time is not convenient then you can listen to the teaching and the midrash after on our YouTube channel.

What are we doing and why do we teach this way?

We are going to discuss both sides of an issue and then let you choose. It is the work of the Ruach (Spirit) to direct and to teach you.

The medieval commentator Rashi wrote that the Hebrew word for wrestle (avek) implies that Jacob was “tied”, for the same word is used to describe knotted fringes in a Jewish prayer shawl, the tzitzityot. Rashi says, “thus is the manner of two people who struggle to overthrow each other, that one embraces the other and knots him with his arms”.

Our intellectual wrestling has been replaced by a different kind of struggle. We are wrestling with Yehovah as we grapple with His Word. It is an intimate act, symbolizing a relationship in which Yehovah and you and I are bound together. My wrestling is a struggle to discover what Yehovah expects of us, and we are “tied” to the One who assists us in that struggle.

Today, many say Israel means “Champion of God”, or better — the “Wrestler of God”.

Our Torah sessions each Shabbat teaches you and encourages you to constantly challenge, question, argue against, as well as view alternative views and explanations of the Word. In other words, we are to “wrestle with the Word” to get to the truth. Jews worldwide believe that you need to wrestle with the Word and constantly challenge Dogma, Theology, and views or else you will never get to the Truth.

We are not like most churches where “The preacher talks and everyone listens.” We encourage everyone to participate, to question and to contribute what they know on the subject being discussed. We want you to be a champion wrestler of the Word of Yehovah. We want you to wear the title of Israel, knowing that you not only know but are capable of explaining why you know the Torah to be true with logic and facts.

We have a few rules though. Let others talk and listen. There is no discussion about UFO’s, Nephilim, Vaccines or conspiracy-type subjects. We have people from around the world with different world views. Not everyone cares who is the President of any particular country. Treat each other with respect as fellow wrestlers of the word. Some of our subjects are hard to understand and require you to be mature and if you do not know, then listen to gain knowledge and understanding and hopefully wisdom. The very things you are commanded to ask Yehovah for and He gives to those who ask.

Jas 1:5 But if any of you lacks wisdom, let him ask of God, who gives to all liberally and with no reproach, and it shall be given to him.

We hope you can invite those who want to keep Torah to come and join us by hitting the link below. It is almost like a Torah teaching fellowship talk show with people from around the world taking part and sharing their insights and understandings.

We start off with some music and then some prayers and it’s as though you were sitting around the kitchen back in Newfoundland having a cup of coffee and all of us enjoying each other’s company. I hope you will grace us with your company someday.

Sabbath services begin at 12:30 PM EDT where we will be doing prayers, songs and teaching from this hour.

Shabbat midrash will begin at about 1:15 pm Eastern.

We look forward to you joining our family and getting to know us as we get to know you.

Joseph Dumond is inviting you to a scheduled Zoom meeting.

Topic: Joseph Dumond’s Personal Meeting Room

Meeting ID: 350 585 5877

One tap mobile

+13017158592,,3505855877# US (Germantown)

+13126266799,,3505855877# US (Chicago)

Dial by your location

+1 301 715 8592 US (Germantown)

+1 312 626 6799 US (Chicago)

+1 346 248 7799 US (Houston)

+1 669 900 6833 US (San Jose)

+1 929 436 2866 US (New York)

+1 253 215 8782 US (Tacoma)

We read through the entire Torah along with the Prophets and the New Testament once over the course of 3 1/2 years. Or according to the Sabbatical Cycle which means we read it all twice over a 7-year period. This allows us to cover more in-depth rather than being rushed to cover as much as is covered on an annual basis. We allow all to comment and take part in the discussions.

Septennial Torah Portion

If you go to Torah Portion in our archived section, you can then go to the 1st year, which is the 1st year of the Sabbatical Cycle, the one we are in now, as we state at the top of every Newsletter. There, you can scroll down to the proper date and see that this Shabbat, we could very well be midrashing about:

Numbers 6

Job 11-14

Hebrews 5-6

We are in the 1st Sabbatical Cycle in 2024-2025. We go through the entire Bible twice in a 7 year cycle. This means we cover the entire Bible once every 3 1/2 years. It gives us more time to debate and discuss each portion we read.

If you missed last week’s exciting discoveries as we studied that section, you can go and watch past Shabbats on our media section.

New Moon Sunday Night?

New Moon Sunday Night?

The new moon is expected to be seen this coming Sunday. Take your family out and see who can see it first after the sunset. Write me in the comments and let us know who saw it first and where you saw it from.

By doing this simple commandment, you will be teaching yourself one of the biggest lessons about the Holy Days. So be a doer and go out and look and learn why nobody can know the day or the hour.

We are in Trouble!!

We are in Trouble!!

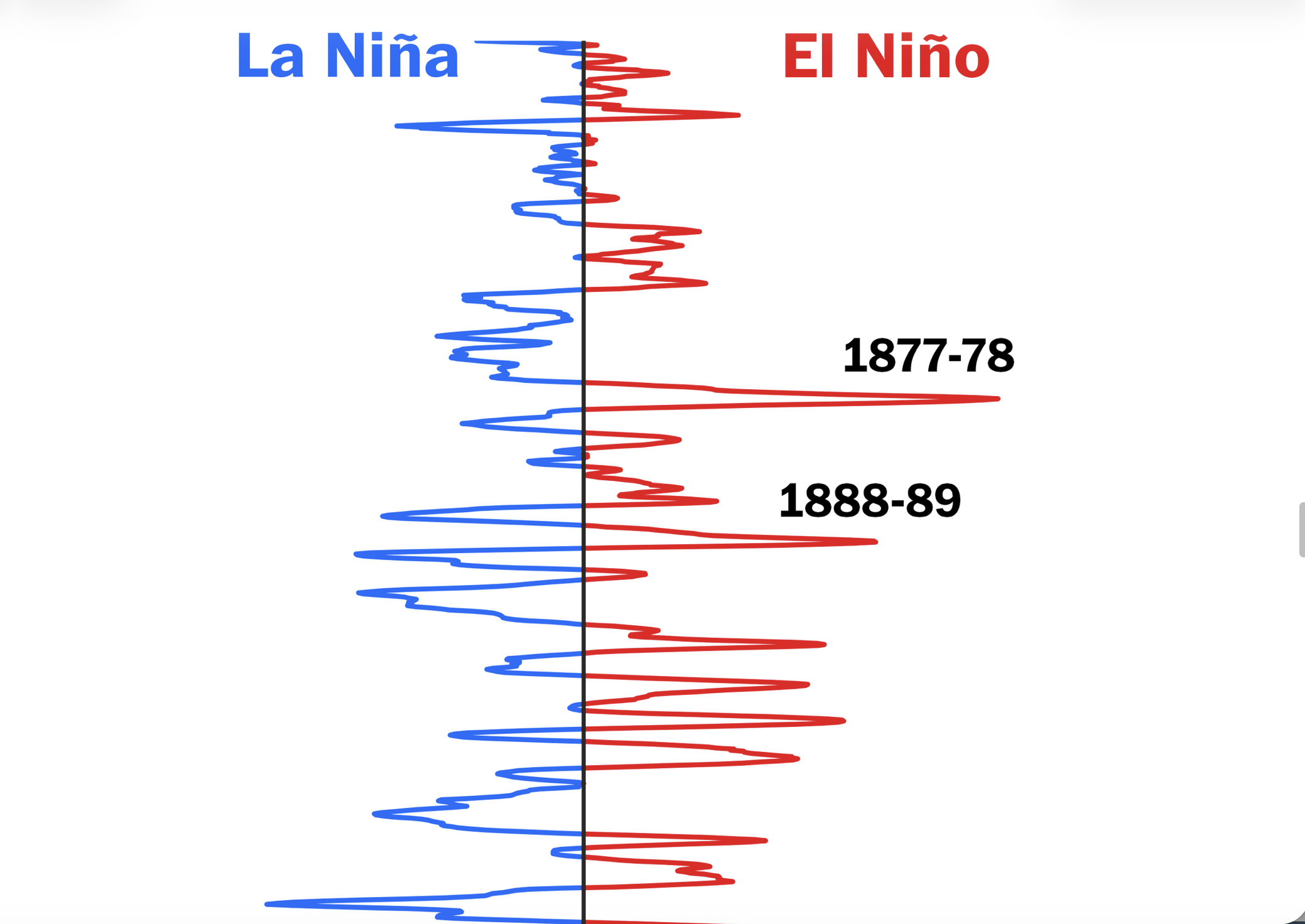

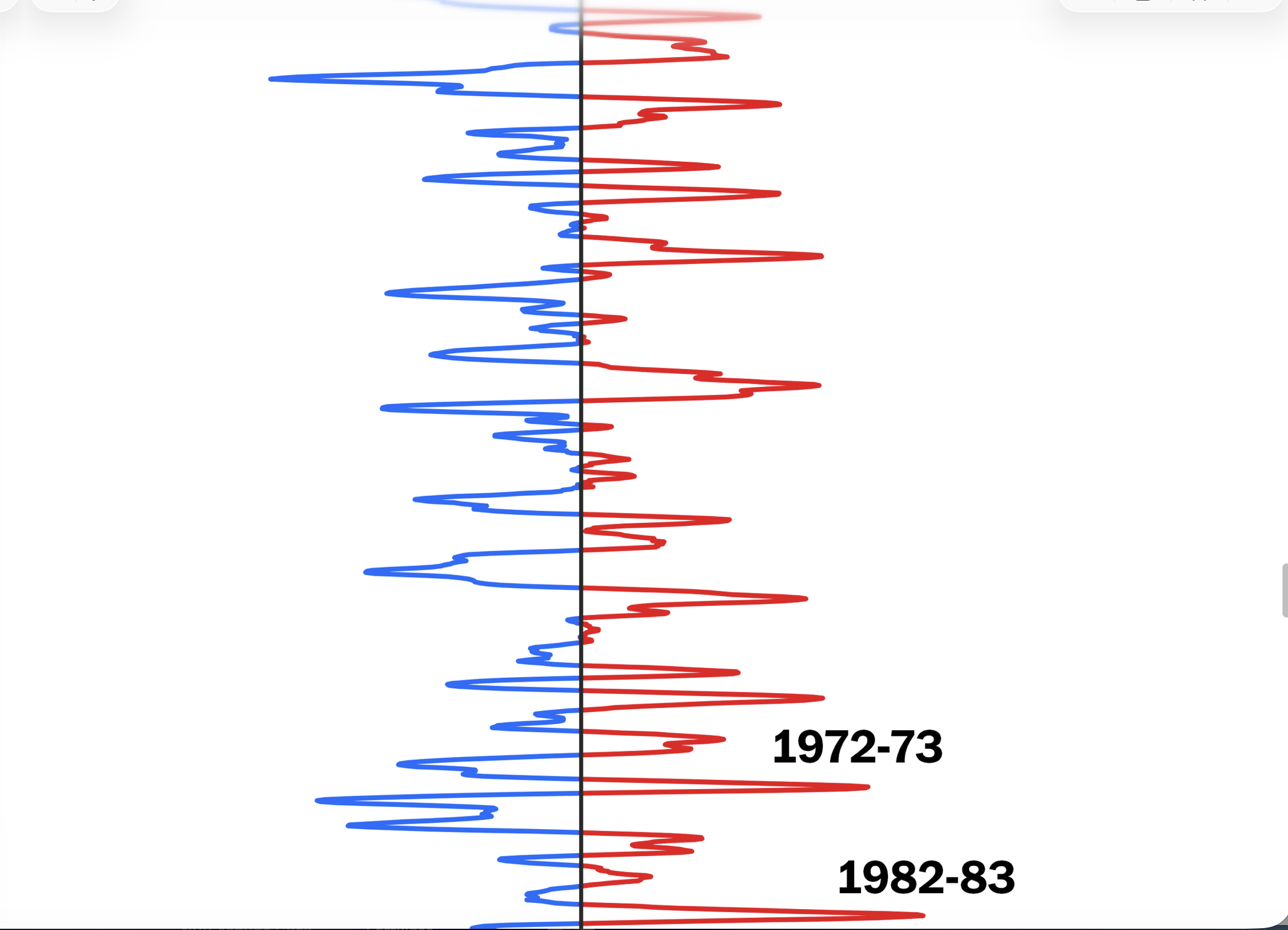

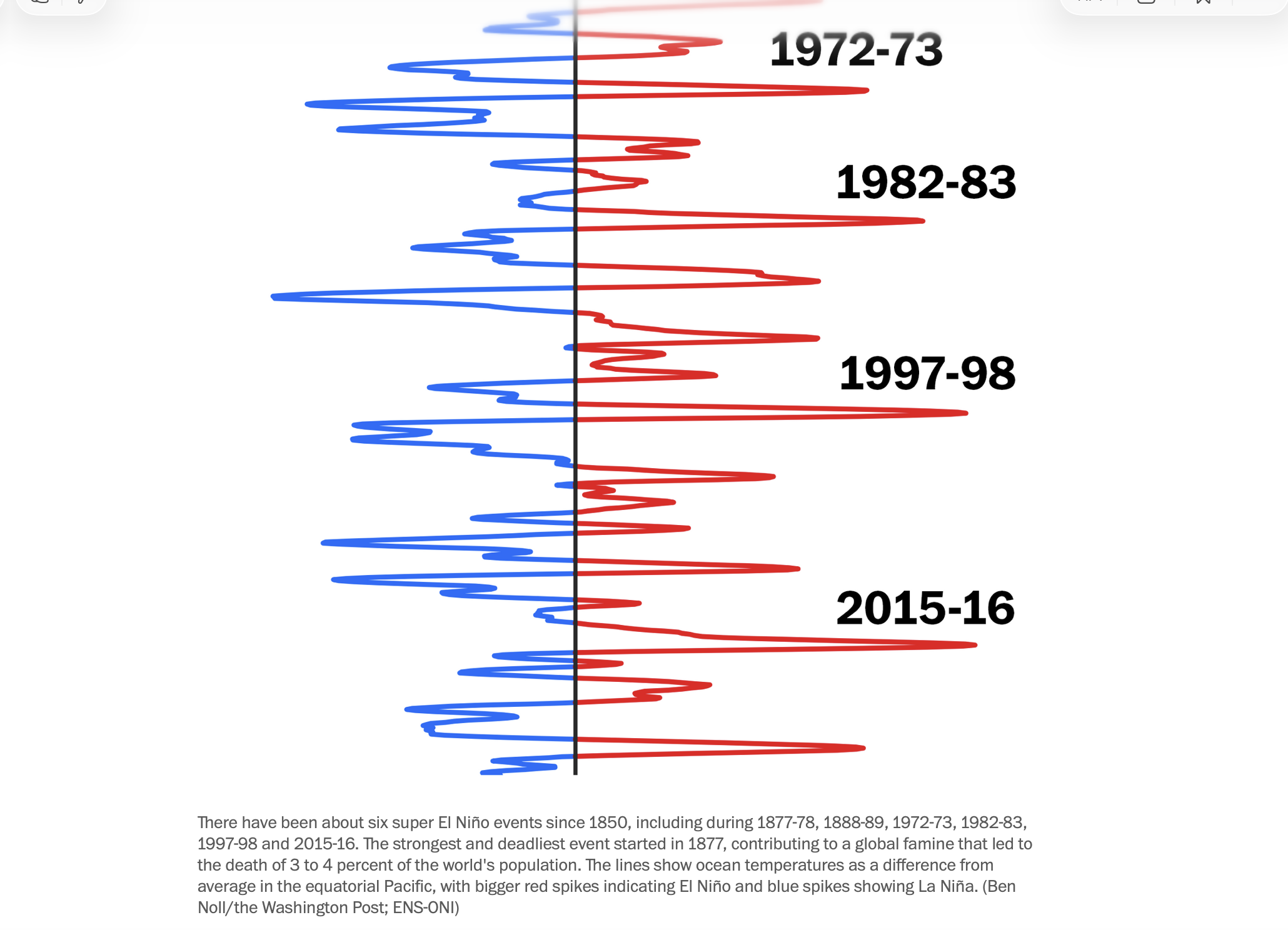

The 1875–1878 El Niño and the Great Global Drought and Famine

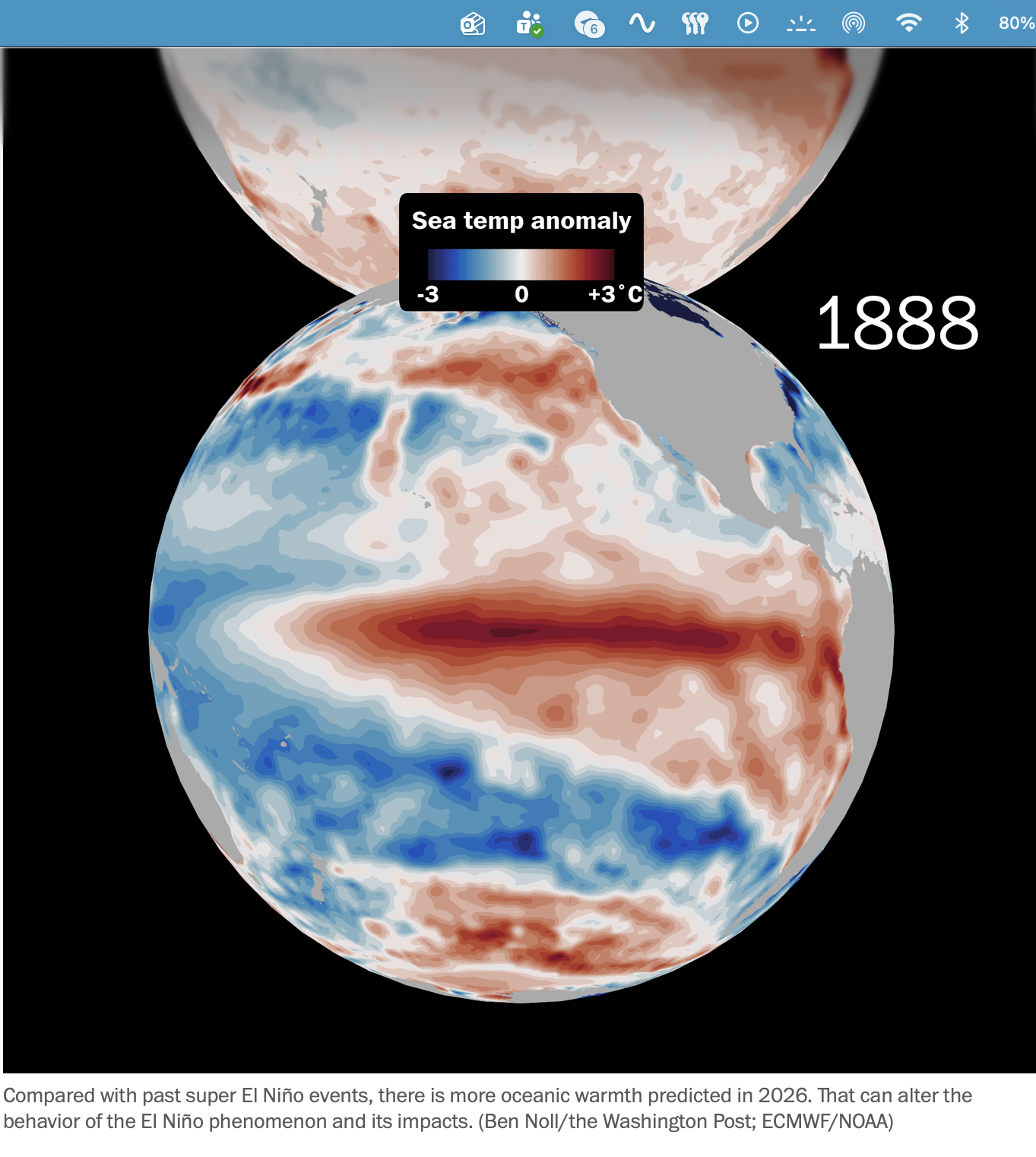

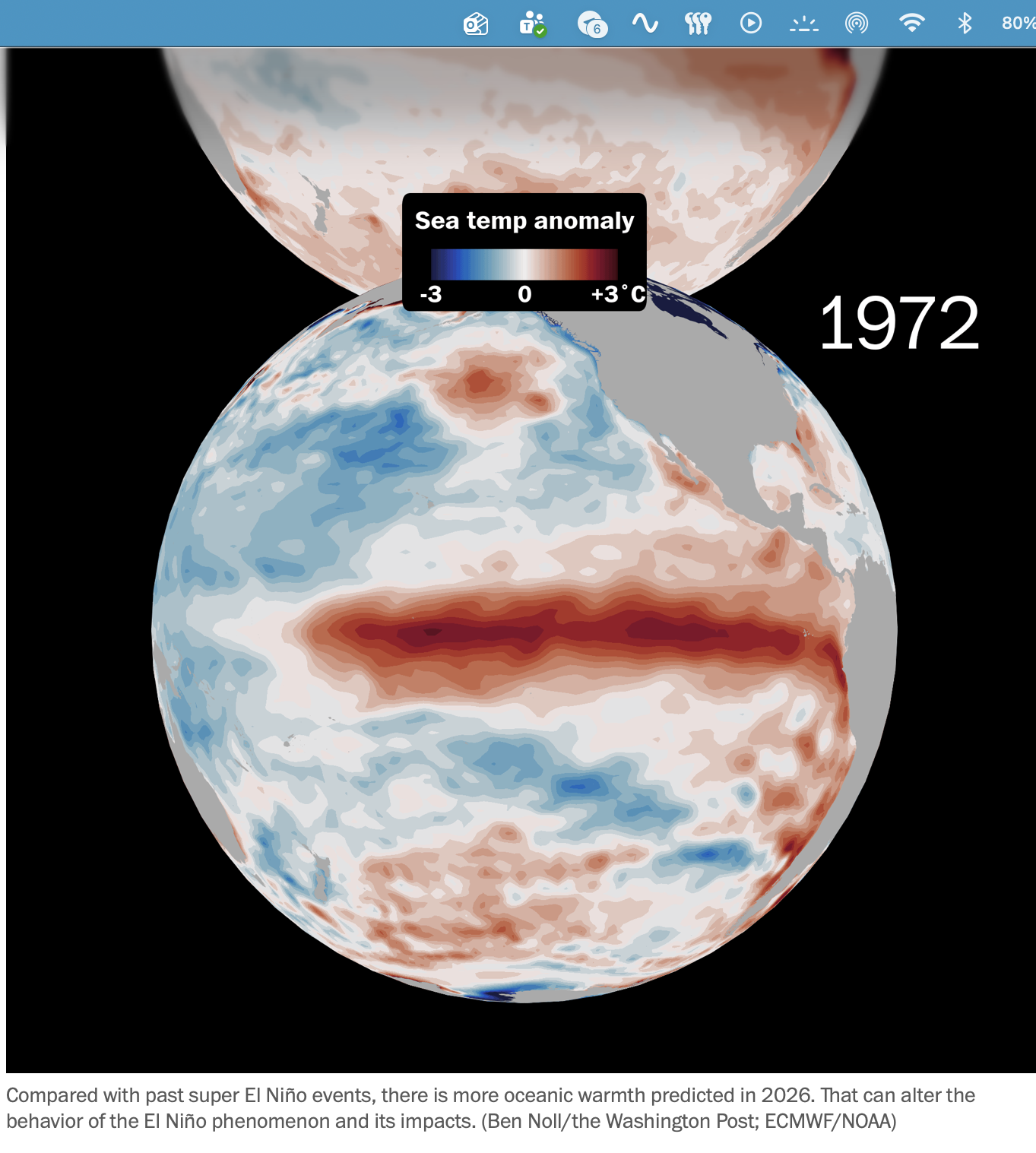

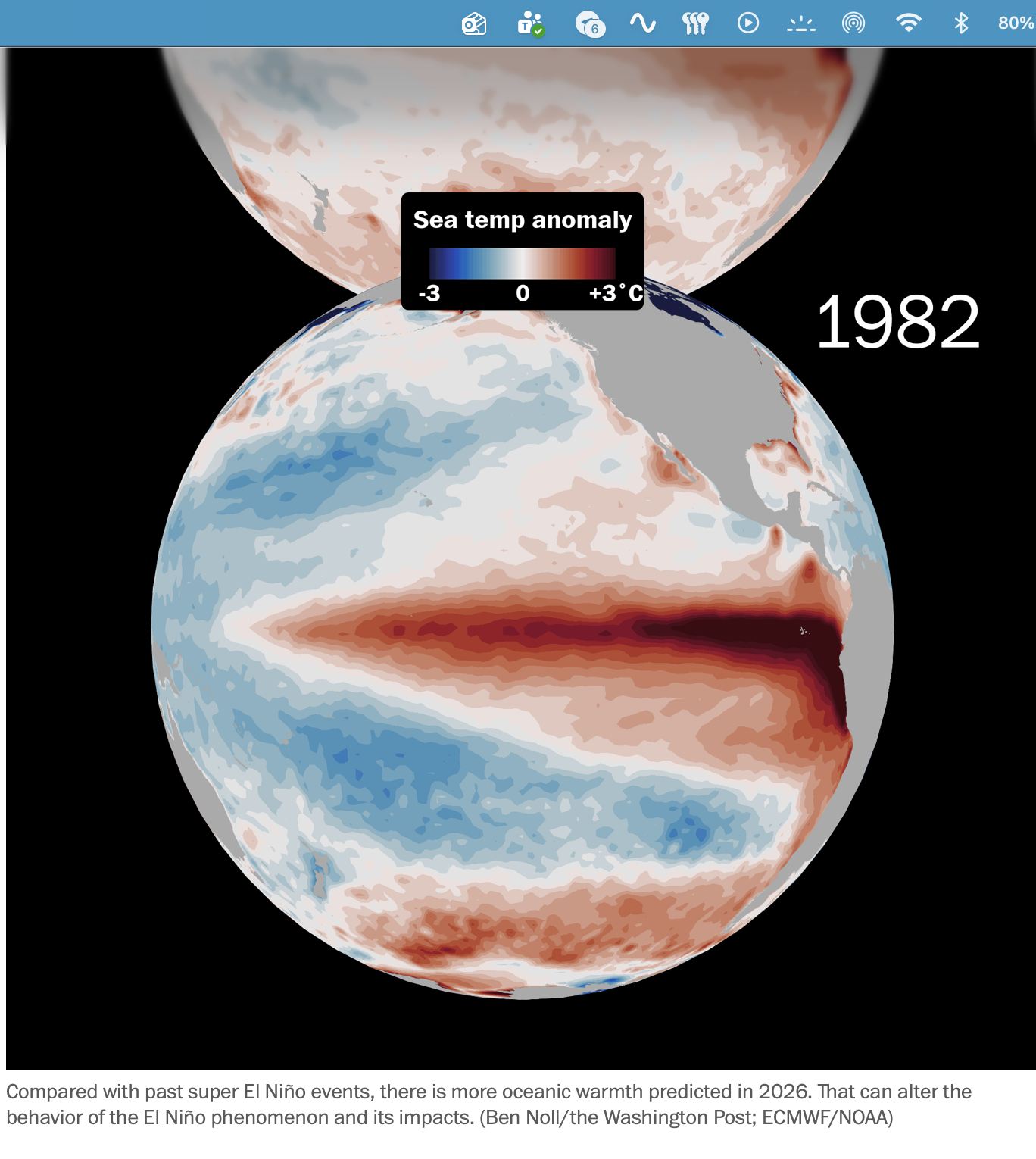

Between 1875 and 1878, the world experienced one of the most catastrophic climate-driven disasters in recorded history — arguably the worst environmental disaster to ever befall humanity. At its heart was an exceptionally powerful and prolonged super El Niño that peaked in 1877–1878. Scientists consider this event among the strongest on record, rivaling or exceeding modern super El Niños such as 1982–83, 1997–98, or 2015–16. It lasted 16–18 months and was dramatically amplified by a record-strong positive Indian Ocean Dipole in 1877 and unusually warm North Atlantic conditions in 1878. These forces flipped the Pacific from a preceding cool, La Niña-like phase into extreme warming, shattering global monsoon systems.

The result was the Great Global Drought of the 1870s, which struck simultaneously across multiple continents and both hemispheres. Asia was hit hardest: near-total monsoon failures devastated India’s Deccan Plateau and southern regions for multiple seasons, while northern China suffered catastrophic dryness. Brazil’s semiarid Nordeste endured the “Grande Seca,” and droughts ravaged parts of Africa, Australia, and Southeast Asia. Crop failures were total and prolonged — rice, wheat, maize, and other staples collapsed across vast regions. Paleoclimate reconstructions describe this as the most intense and extensive drought in at least the past 800 years in Asia, with comparable severity elsewhere.

The human toll was staggering. The Great Famine of 1876–1878 killed an estimated 30–60 million people worldwide — more than 50 million by the most commonly cited figures — roughly 3–4% of the global population of 1.3–1.4 billion at the time. That death toll would equal at least 250 million people if it occurred today. Breakdowns include 5.5–12 million (or higher) in India, 9.5–13 million (up to 19–30 million in broader estimates) in northern China, and hundreds of thousands to 2 million in Brazil, plus millions more across Africa and other zones. Starvation was worsened by epidemics, mass migrations, and social collapse.

In India, British colonial policies — continued grain exports during shortages, minimal and inhumane relief (such as the punitive “Temple wage” labor camps), and the dismantling of traditional resilience systems — dramatically amplified the crisis. As researcher Deepti Singh has noted, famines are not an inevitable result of drought; deliberate human actions turned a severe climate event into one of history’s greatest tragedies. Historian Mike Davis’s Late Victorian Holocausts powerfully documents how natural catastrophe and imperial mismanagement converged to shape long-term global inequalities. Florence Nightingale described the suffering in India as “such a hideous record of human suffering and destruction the world has never seen before.”

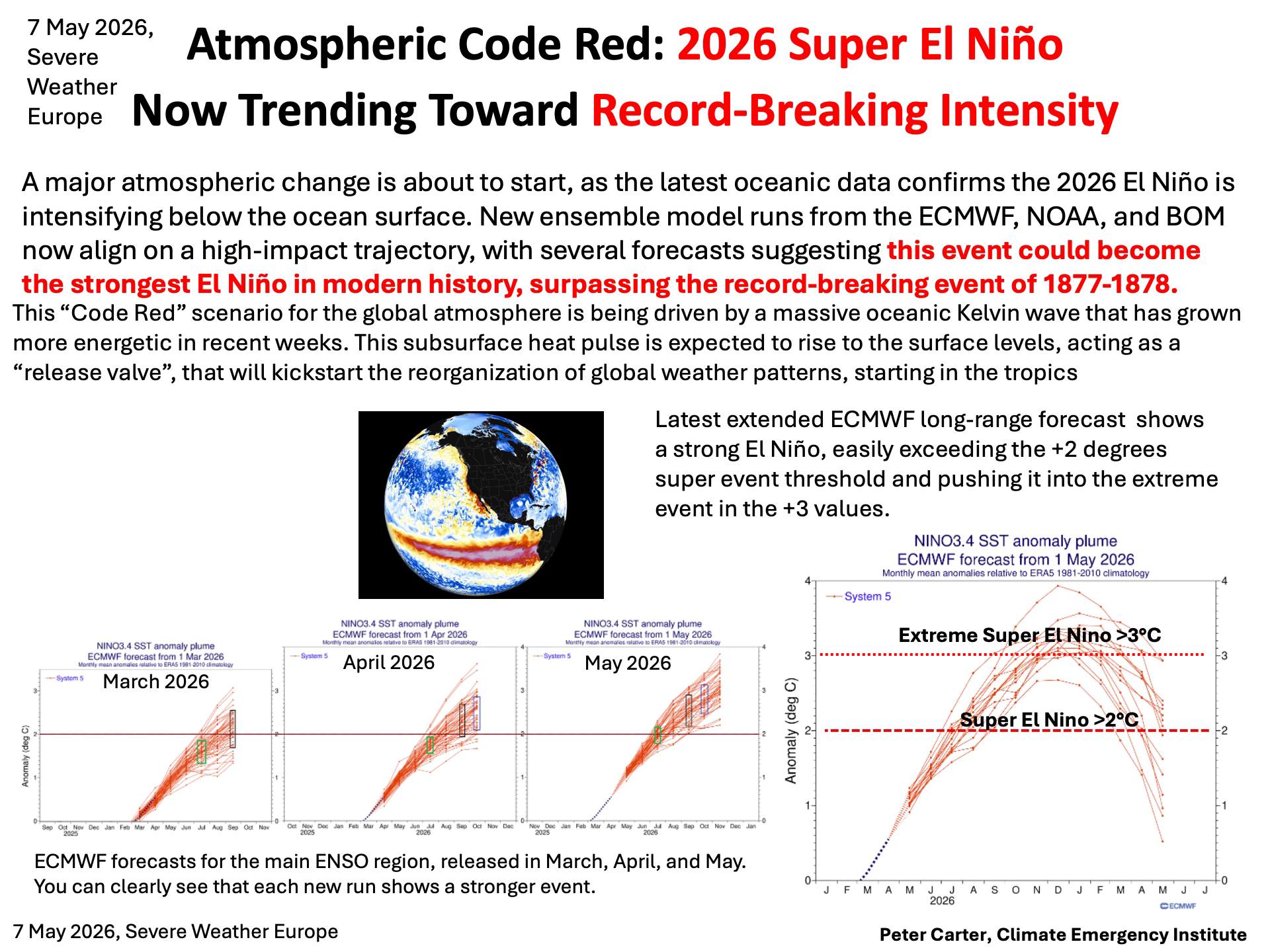

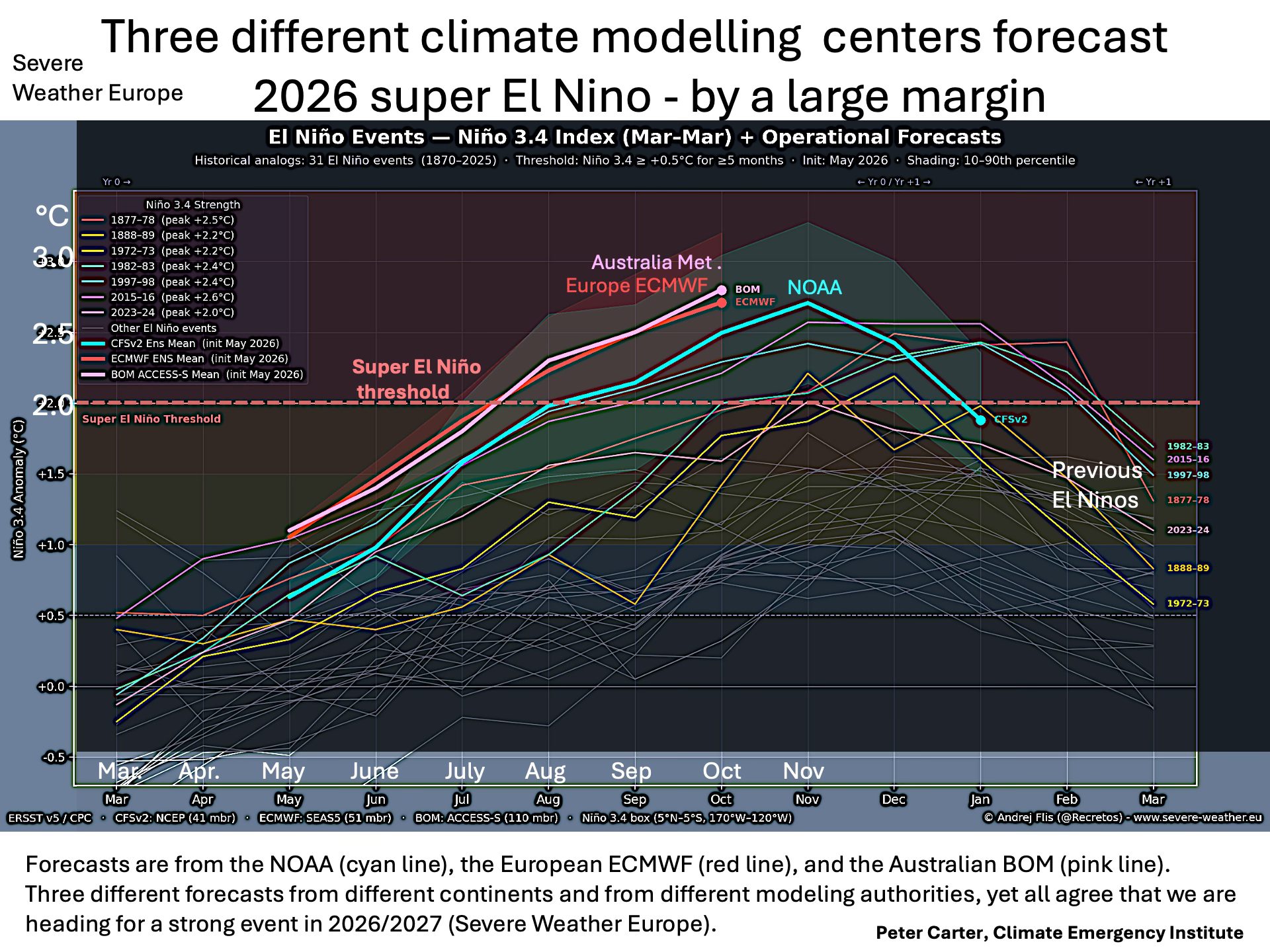

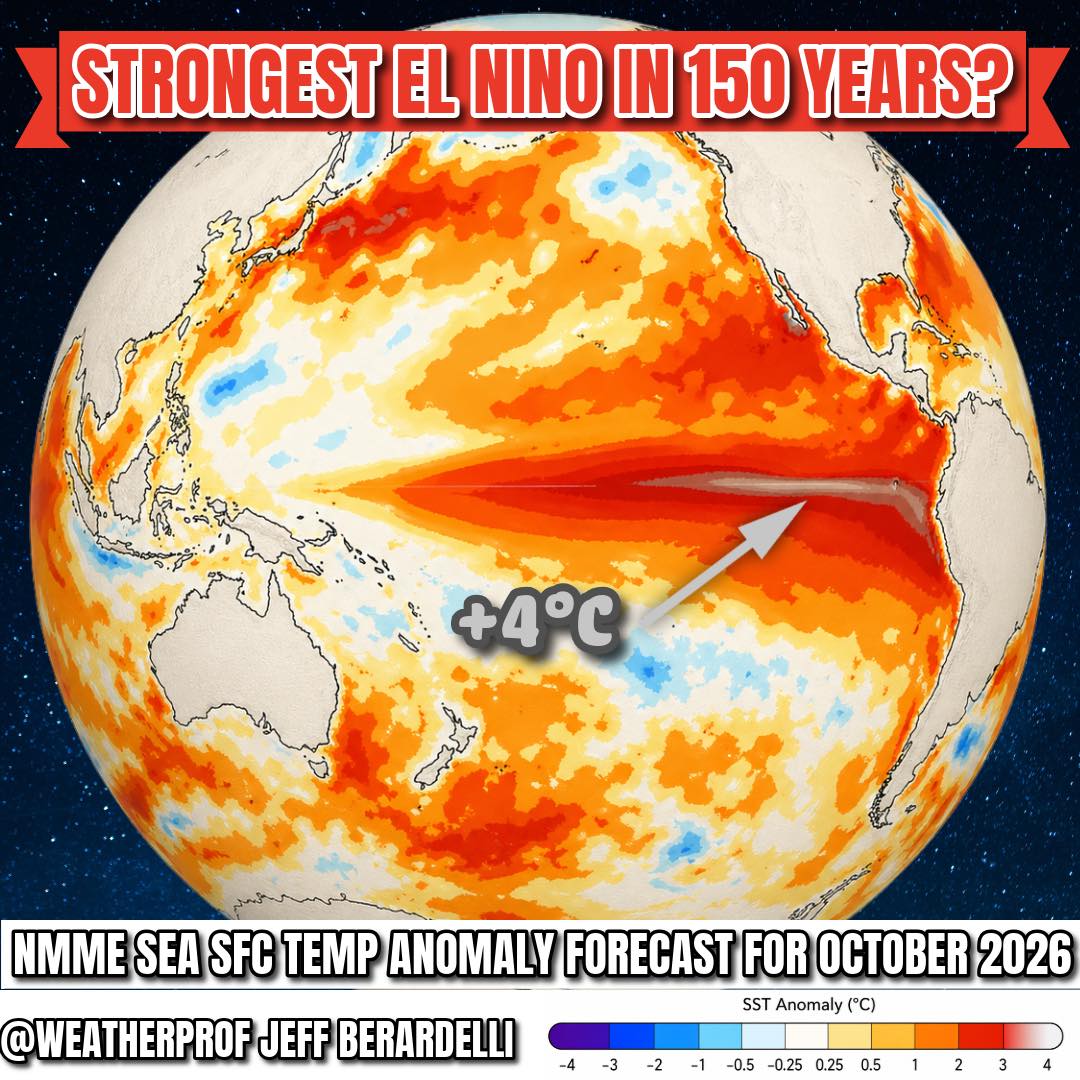

Projected Consequences of the Developing 2026 El Niño, Compounded by Biblical Prophecy of the Two Witnesses (Fall 2026–Fall 2029)

As of May 2026, a strong El Niño is developing rapidly in the tropical Pacific. Forecasts show a high probability (60%+) of it strengthening through late 2026 and reaching super-El Niño intensity (Niño 3.4 anomalies potentially +2°C to +3°C or higher) by winter 2026–2027. Ocean temperatures could surge as much as 3°C (5.4°F) above average, potentially breaking records.

Climate change has raised the baseline: our atmosphere and oceans are substantially warmer than in the 1870s, meaning associated extremes could be even more severe. Our global population of over 8 billion and tightly interconnected supply chains heighten the vulnerability. While modern monitoring and prediction systems (greatly improved since the pivotal 1982–83 super El Niño, with thousands of buoys, satellites, and advanced models from NOAA and ECMWF) give us far better warnings than in 1877, significant risks remain.

The situation becomes far more serious when we overlay biblical prophecy. In Revelation 11, the Two Witnesses begin their 1,260-day (three-and-a-half-year) ministry in the fall of 2026 and are granted power to shut up the sky so that no rain falls during their prophesying. This divinely ordained drought would overlap and dramatically extend the El Niño-driven dryness through roughly fall 2029 — creating a multi-year global rainfall shutdown without modern precedent.

Here is the likely step-by-step progression through 2030 (probabilistic, based on climate models, historical analogs, and the added prophetic factor):

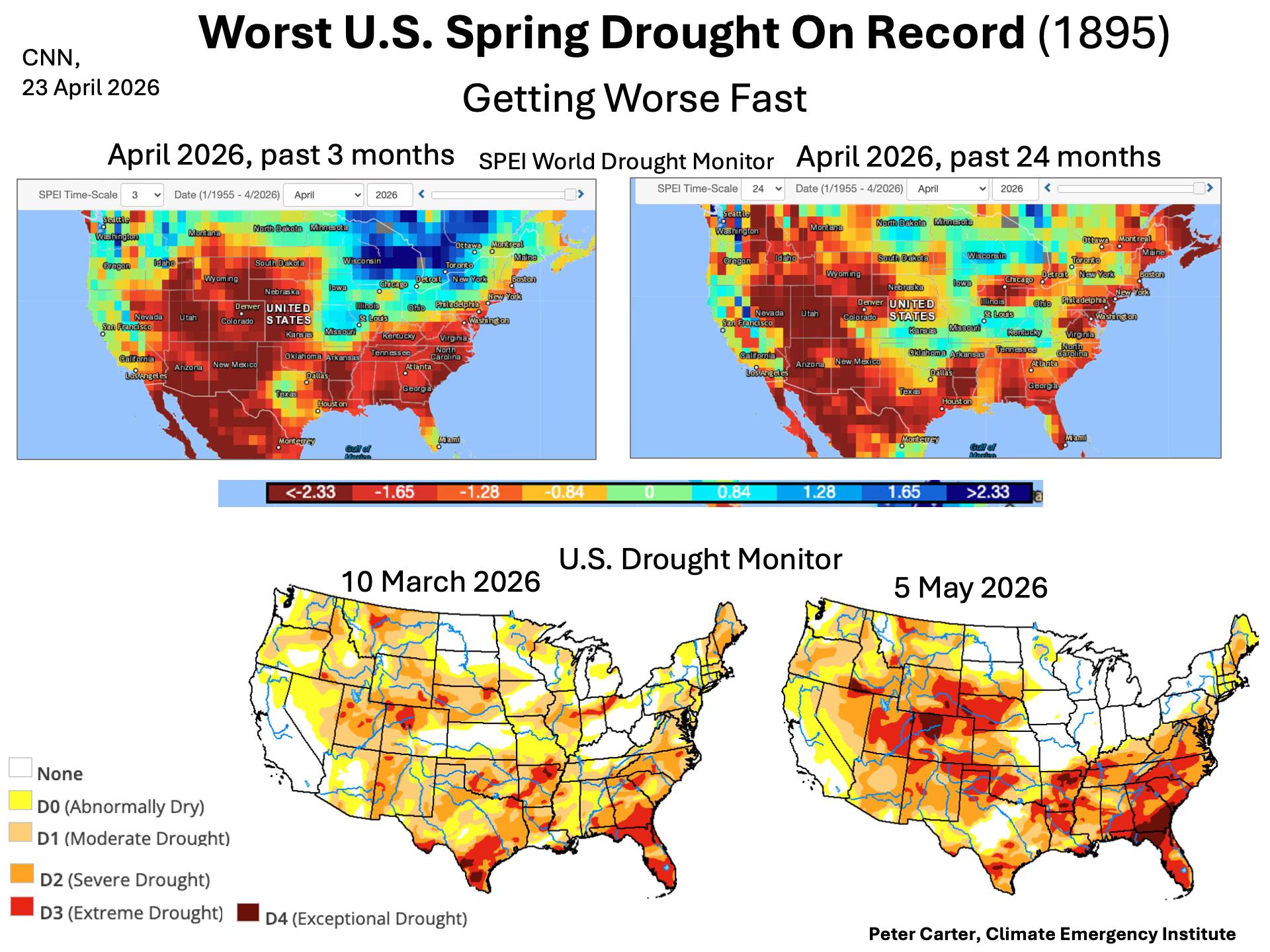

Late 2026 (Onset and Early Build-Up): Early drought risks rise across India, Southeast Asia, Australia, southern/eastern Africa, Brazil’s Nordeste, and northern China, while floods increase in Peru, Ecuador, East Africa, and parts of the western U.S. Global temperatures push 2026 among the warmest on record. Drought initially affects 15–20% of global cropland. Food prices rise 5–10% globally; fuel/energy prices climb 5–8%. The Two Witnesses begin in fall 2026, accelerating dryness. Food insecurity rises for 100–200 million.

2027 (Peak Intensity): Record global heat, with some months potentially exceeding +2°C above pre-industrial. Severe synchronized droughts could cover 25–35%+ of harvested areas as the no-rain period locks in. Crop failures intensify across Asia, Africa, South America, and Australia. Food commodity prices surge 20–50% (rice and wheat potentially doubling in hard-hit regions), with overall food inflation of 15–30%+ in vulnerable countries. Fuel prices rise sharply. Famine and acute food insecurity could threaten 500 million to over 1 billion people, with potential death tolls of 10–30 million in worst-case scenarios. Migration, disease outbreaks, and trillions in economic losses follow.

2028–2029: El Niño fades, but the Three-Year Drought from the Two Witnesses continues. Lingering dryness affects 20–30% of croplands. Food prices stay elevated at 15–40%. Cumulative impacts mount.

2029–2030: The no-rain period ends around fall 2029. Drought eases but ecosystem damage remains. Food prices stabilize 10–25% above 2025 levels. Total famine-related deaths across the period could reach 20–50 million or higher in compounding scenarios. As Deepti Singh warns, enhanced drought risk will threaten food, water, and economic security in vulnerable regions, with effects cascading globally across interconnected systems. International collaboration will be vital.

Modern tools give us better preparation than in 1877, but the convergence of a potential super El Niño with the prophesied Three-Year Drought would still test civilization severely.

These projections are probabilistic, based on current scientific models, historical precedents, and the specified biblical factor. Actual outcomes will depend on the exact strength of the El Niño, human preparedness, international aid coordination, and technological interventions (early warnings, drought-resistant crops, and desalination). Modern monitoring offers far better tools than in the 1870s, yet the scale of a three-year global rain cessation would test civilization in ways never before seen. For the latest official outlooks, consult NOAA, the World Meteorological Organization, or ECMWF updates, and consider theological perspectives alongside scientific ones for a complete picture.

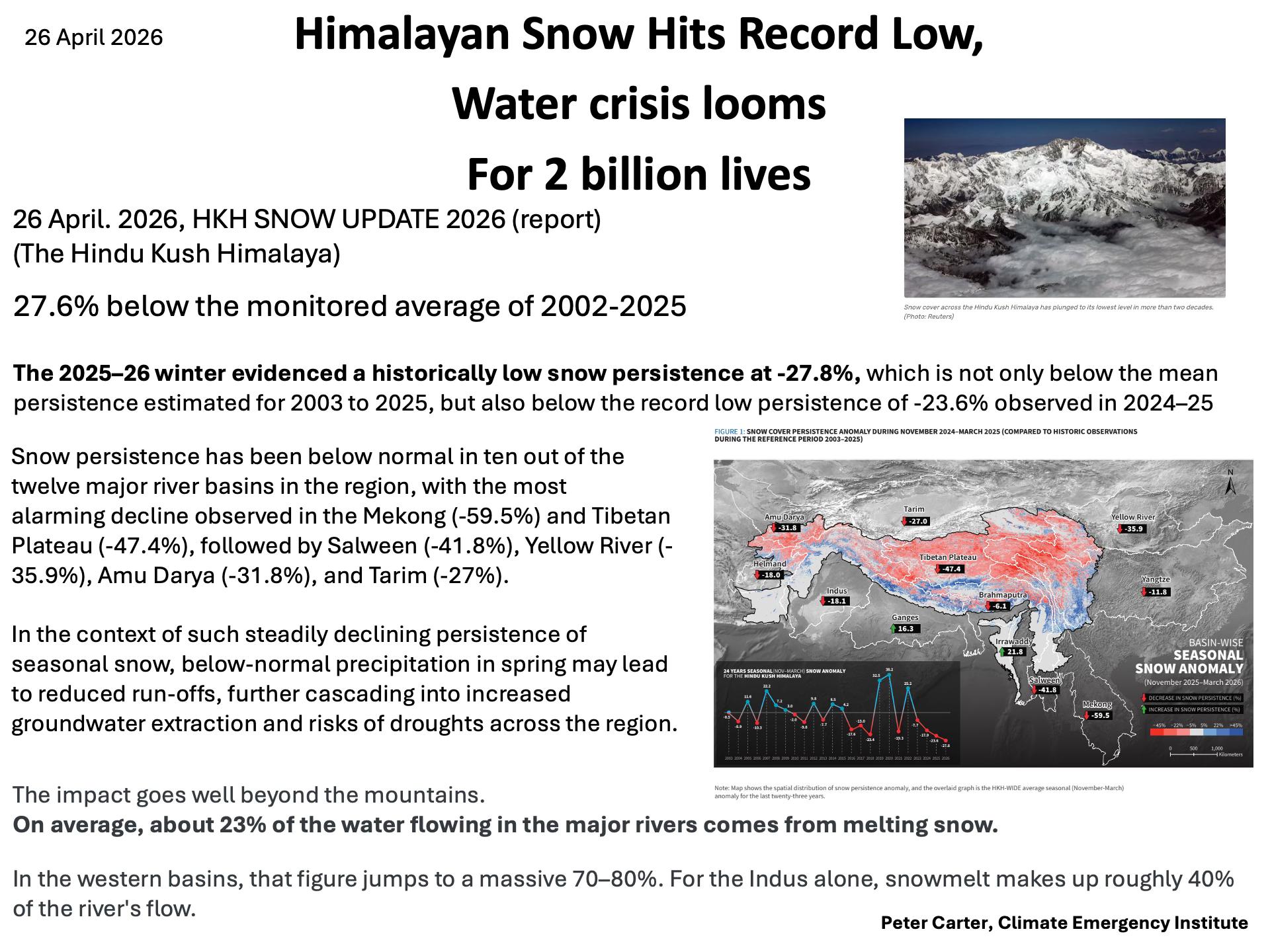

The lack of snow in the Himalayas (Hindu Kush Himalaya or HKH region) is extremely severe right now — a record low for the fourth consecutive year.

The Himalayan Snow Drought — The Water Tower of Asia Is Running Dry

This photo aligns with the latest April 2026 ICIMOD Snow Update Report 2026. It highlights a dramatic decline: snow persistence (how long snow stays on the ground) across the HKH is 27.8% below the long-term average — the lowest in over 20–24 years of monitoring. This continues a worrying multi-year trend of “snow drought.”

Why This Is So Bad

Snowpack acts as the “water tower of Asia”: Seasonal snow slowly melts and feeds rivers through spring and summer. With far less snow accumulated this winter (November 2025–March 2026), the slow-release water supply is critically reduced.

10 out of 12 major river basins are below normal. Sharpest drops include the Mekong (60% below), Tibetan Plateau (>47%), and notable deficits in the Indus, Brahmaputra, Salween, Yellow River, and others. The Ganges basin was one of the few with a slight increase (16%), but overall the region is in deficit.

Compounding factors: Warmer temperatures (elevation-dependent warming) turn potential snow into rain at mid-elevations, accelerate melt of whatever snow does fall, and speed up glacier retreat (already losing ice at double the rate since 2000).

Impacts on Major Rivers and Downstream Areas

The Himalayas feed 12 major river systems (including Indus, Ganges, Brahmaputra, Mekong, Yangtze, Salween, etc.), supporting drinking water, irrigation, hydropower, and ecosystems for nearly 2 billion people across South Asia, Southeast Asia, and Central Asia.

Reduced spring/summer flows: Snowmelt normally provides ~23–25% of annual river runoff (higher in western basins like the Indus). Expect lower river levels, especially early in the melt season, leading to water shortages.

Agriculture and food security: Millions of farmers face drier fields, reduced irrigation, and lower crop yields (rice, wheat, etc.) in the coming months.

Hydropower and energy: Dams and plants reliant on steady flows (common in India, Nepal, Pakistan, China) could see reduced output.

Drinking water and ecosystems: Vanishing springs (already reported in Kashmir), drier soils, and stressed wetlands. Increased risk of wildfires, dust, and heat stress.

Broader risks: Greater reliance on erratic monsoons (which are also becoming more unpredictable). Potential for early water stress turning into drought, plus long-term glacier thinning that worsens future years.

This is not a one-off event but part of a systemic shift under warming — the fourth straight year of below-normal snow. Scientists warn of imminent water shortages this spring/summer if the trend holds.

In the context of the broader 2026 super El Niño (and any overlapping factors like the prophetic no-rain scenario discussed earlier), this Himalayan snow deficit could amplify regional dryness and food/price pressures significantly. Local reports (e.g., Kashmir) already note dry taps and stressed orchards.

For the most current satellite views or basin-specific data, check ICIMOD.org or regional meteorological agencies.

“Look at the Anna Tower (Anah Tower) in Anah, Iraq — a 92-foot-tall (28-meter) minaret that now serves as a dramatic natural water gauge for the Euphrates River.

In 2021, during higher water levels, the river reached right up to the base of the tower, surrounding the lower structure.

Today in 2026, the water has dropped more than 25 to 35 feet (8–11 meters) below that same base. Large sections of the riverbed are completely exposed and dry — you can clearly see how far the level has fallen. The current depth in the main channel near the tower is critically low, often less than 10–15 feet (3–5 meters) in many places.

To put this in perspective: From the 1988-style historical peak (potentially halfway or more up the tower) to today, the total drop could be 50–70+ feet in extreme flood-to-drought swings.

The Euphrates originates in the mountains of eastern Turkey (the Armenian Highlands and Taurus Mountains). This year’s snowpack in those headwaters was significantly below average, with reduced winter snowfall and faster melt due to warmer temperatures — meaning far less spring and summer runoff is feeding the river as it flows through Syria and into Iraq.

This is the same Euphrates the Bible says will one day dry up enough for armies to cross on dry ground (Revelation 16:12). The Anna Tower shows us just how far it has already dropped — and how little water is left.”

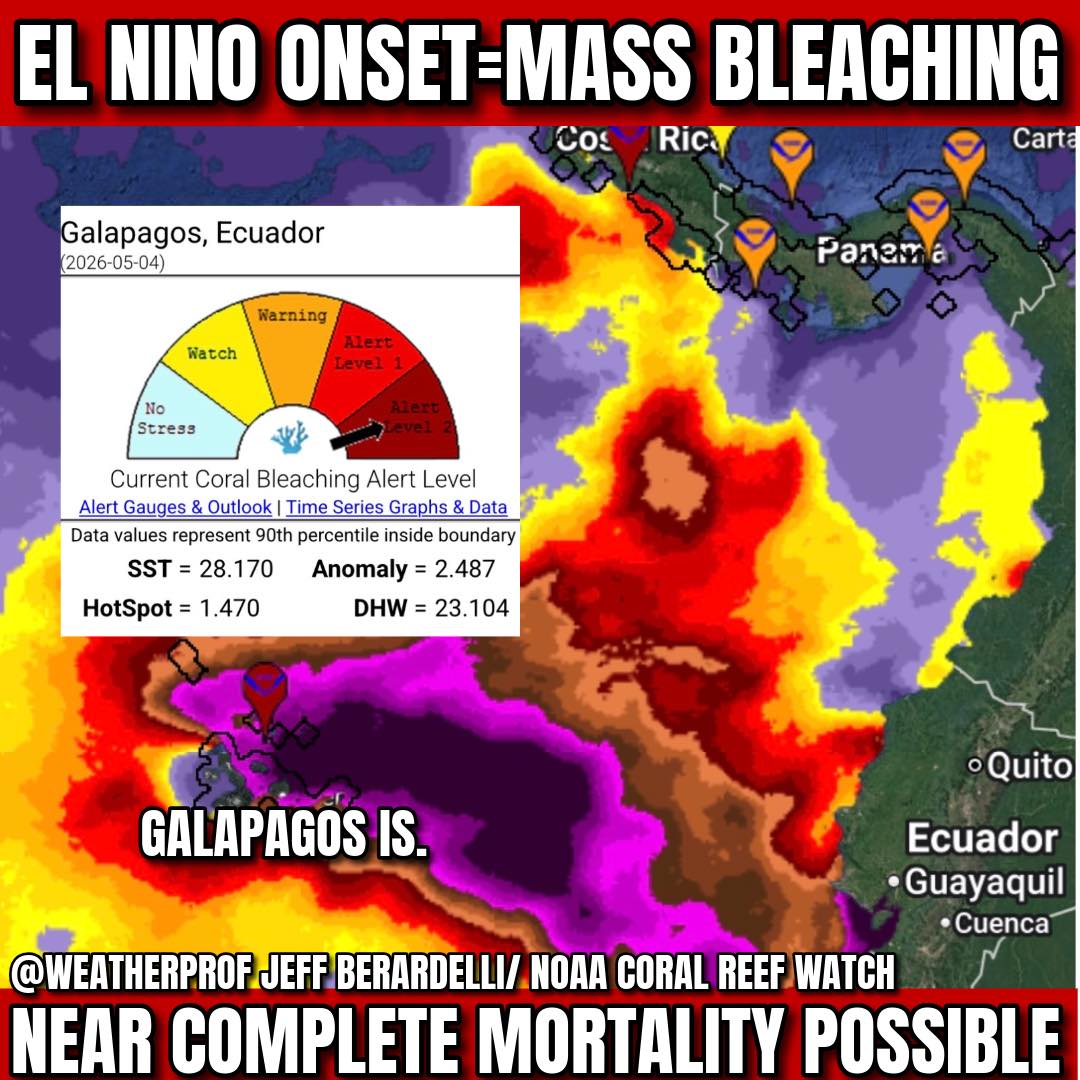

Galápagos in Crisis

El Niño and the Revelation Prophecy of the Seas Turning to Blood

As we shared in last week’s Newsletter (“The 40 Days After Shavuot”), a potentially very strong El Niño is developing in the Pacific for late 2026. Meteorologist Jeff Berardelli recently highlighted the growing emergency: sustained marine heat stress has now reached 20+ weeks in the waters around the Galápagos Islands. NOAA’s Coral Reef Watch warns this level means “Near Complete Mortality” of shallow-water coral reefs.

The Galápagos Penguins — already listed as endangered with only a few thousand left — are facing a life-threatening event. These birds rely on the cold, nutrient-rich upwelling of the Cromwell Current to bring fish to the surface. When El Niño warms surface waters by +5–10°F, that upwelling shuts down like a lid on a pot. The entire food chain collapses: phytoplankton dies off, fish disappear, and predators starve.

This is not theory. The 1982–83 super El Niño killed 77% of the Galápagos penguin population. The 1997–98 event caused a similar ~65% crash. Scientists describe it as a cascade: primary productivity collapses, and the ecosystem sickens from the bottom up.

The Galápagos Islands are the living laboratory that helped inspire Charles Darwin’s theory of evolution — a place of unparalleled biodiversity found nowhere else on earth. Now that same unique ecosystem is under severe stress.

The Revelation Connection: Waters Turning to Blood and Fish Dying

This brings us to one of the most sobering prophecies in the Book of Revelation.

In the second trumpet judgment (Revelation 8:8-9):

“The second angel sounded his trumpet, and something like a huge mountain, all ablaze, was thrown into the sea. A third of the sea turned into blood, a third of the living creatures in the sea died, and a third of the ships were destroyed.”

And again in the second bowl judgment (Revelation 16:3):

“The second angel poured out his bowl on the sea, and it turned into blood like that of a dead person, and every living thing in the sea died.”

Many readers have asked: Could the increasing intensity of El Niño events be connected to this prophecy?

Not a literal fulfillment yet — we have not seen one-third of the world’s oceans turn to literal blood. But we are watching a powerful shadow and precursor of exactly what John described.

During strong El Niño events, scientists have documented massive harmful algal blooms (red tides) that literally turn stretches of ocean reddish-brown and kill huge numbers of fish and marine life. The warm, stagnant waters create perfect conditions for these toxic blooms. The result? Dead fish washing ashore by the thousands, oxygen-depleted “dead zones,” and entire food webs collapsing — precisely the imagery of “the sea turned into blood” and “every living thing in the sea died.”

What we are seeing in the Galápagos right now is a localized but dramatic picture of that judgment: waters that can no longer sustain life, coral reefs dying en masse, and iconic species like the penguins facing starvation.

Why This Matters in the Sabbatical and Jubilee Cycles

As we have been teaching for years, the curses of Leviticus 26 and Deuteronomy 28 intensify as we approach the end of this age. Famine, pestilence, and destruction of the land and seas are part of the warning signs.

El Niño is a natural cycle — but its increasing frequency and severity on top of long-term warming are making each event more destructive. The very mechanisms God built into creation (upwelling, nutrient flows) are being disrupted on a scale that mirrors the judgments written 2,000 years ago.

This is not a coincidence. It is a sign.

The same waters that once teemed with life are now showing us what happens when the life-giving systems are shut off. Just as the Nile turned to blood in Egypt as a judgment, we are seeing pockets of the sea behave the same way today.

The prophecy is clear: one day a third of the sea will turn to blood, and the fish will die on a global scale. What we are seeing in the Galápagos is a warning shot — a small-scale rehearsal so that those with eyes to see will understand the times.

Oil Inventories Plunge Toward “Tank Bottoms”

Oil Inventories Plunge Toward “Tank Bottoms”

Europe in May, U.S. Around July 4

The global oil system is now reaching critical operational limits much faster than most analysts expected.

According to the latest U.S. Energy Information Administration (EIA) Weekly Petroleum Status Report for the week ending May 1, 2026, commercial inventories are drawing down at an alarming pace. Crude oil inventories fell by 2.3 million barrels. Gasoline inventories dropped 2.5 million barrels. Distillate fuel inventories (diesel, heating oil, and jet fuel) fell another 1.3 million barrels, reaching the lowest level since 2005 and sitting approximately 11% below the five-year average for this time of year.

Source: EIA Weekly Petroleum Status Report, released May 6, 2026

Jeff Currie, Senior Advisor at Carlyle Group and one of the most respected commodities analysts in the world, stated on Bloomberg Television on May 6, 2026:

“Europe is going to hit tank bottoms sometime in the month of May… The U.S. is going to hit tank bottoms around July 4th… I’ve never seen anything like it before.”

“Tank bottoms” (also called the operational floor or operational minimums) does not mean the tanks are completely empty. It refers to the point where the remaining usable oil is so low that sediment, water, and sludge at the bottom of the tanks make normal pumping and refining operations extremely difficult or impossible. At that stage, refineries are forced to reduce throughput, costs rise sharply, and supply disruptions become more likely.

Europe is expected to reach these tank bottoms first, sometime in May 2026. The United States is projected to follow closely behind, with tank bottoms likely appearing around July 4, 2026 — or possibly sooner if the current rate of draws continues.

What This Means for Food Prices This Fall in Europe and North America

Diesel is the lifeblood of modern food supply chains. It powers the vast majority of tractors, combines, trucks, trains, refrigerated transport, and much of the fertilizer and chemical logistics that keep food moving from farm to table. When distillate inventories hit these operational floors, diesel prices tend to spike dramatically, and those higher costs flow directly into the price of food.

Europe is expected to feel the pressure first and hardest, beginning as early as this month. North America will follow closely behind starting in July. Higher diesel costs will raise the expense of planting, harvesting, processing, and distributing food across both continents. Grocery prices, already elevated, are likely to rise further and become noticeably more expensive by late summer and into the fall and winter of 2026.

We have been warning about the coming famine since 2005, using the Sabbatical and Jubilee cycles as our guide. What we are seeing now matches exactly the pattern of curses that Yehovah warned Israel about in Leviticus 26:

Lev 26:18And if you will not yet listen to Me for all this, then I will punish you seven times more for your sins.

Lev 26:19And I will break the pride of your power, and I will make your heaven like iron and your earth like bronze.

Lev 26:20And your strength shall be spent in vain. For your land shall not yield its increase, neither shall the trees of the field yield their fruits.

Lev 26:23And if you will not be reformed by Me by these things, but will still walk contrary to Me,

Lev 26:24then I will walk contrary to you and will punish you seven times more for your sins.

Lev 26:25And I will bring a sword on you that shall execute the vengeance of the covenant. And when you are gathered inside your cities, I will send the plague among you. And you shall be delivered into the hand of the enemy.

Lev 26:26When I have broken the staff of your bread, ten women shall bake your bread in one oven, and they shall deliver you your bread again by weight. And you shall eat and not be satisfied.

Lev 26:27And if you will not for all of this listen to Me, but will walk contrary to Me,

Lev 26:28then I will walk contrary to you also in fury. And I, even I, will chastise you seven times for your sins.

Lev 26:29And you shall eat the flesh of your sons, and the flesh of your daughters you shall eat.

These verses describe a time when the land refuses to produce its full increase and food becomes so scarce that even basic baking requires extreme effort and rationing. We are now watching the very mechanisms that can produce this kind of famine being activated in real time: diesel shortages, disrupted global supply chains, and rising costs that will make food more expensive and harder to obtain this fall and winter in Europe and North America.

The systems we depend on for food and fuel are reaching their limits.

Bloomberg Television interview with Jeff Currie (May 6, 2026)

Asian Rice Planting Collapsing

Asian Rice Planting Collapsing

The Famine Warnings of Leviticus 26 Are Now Visible

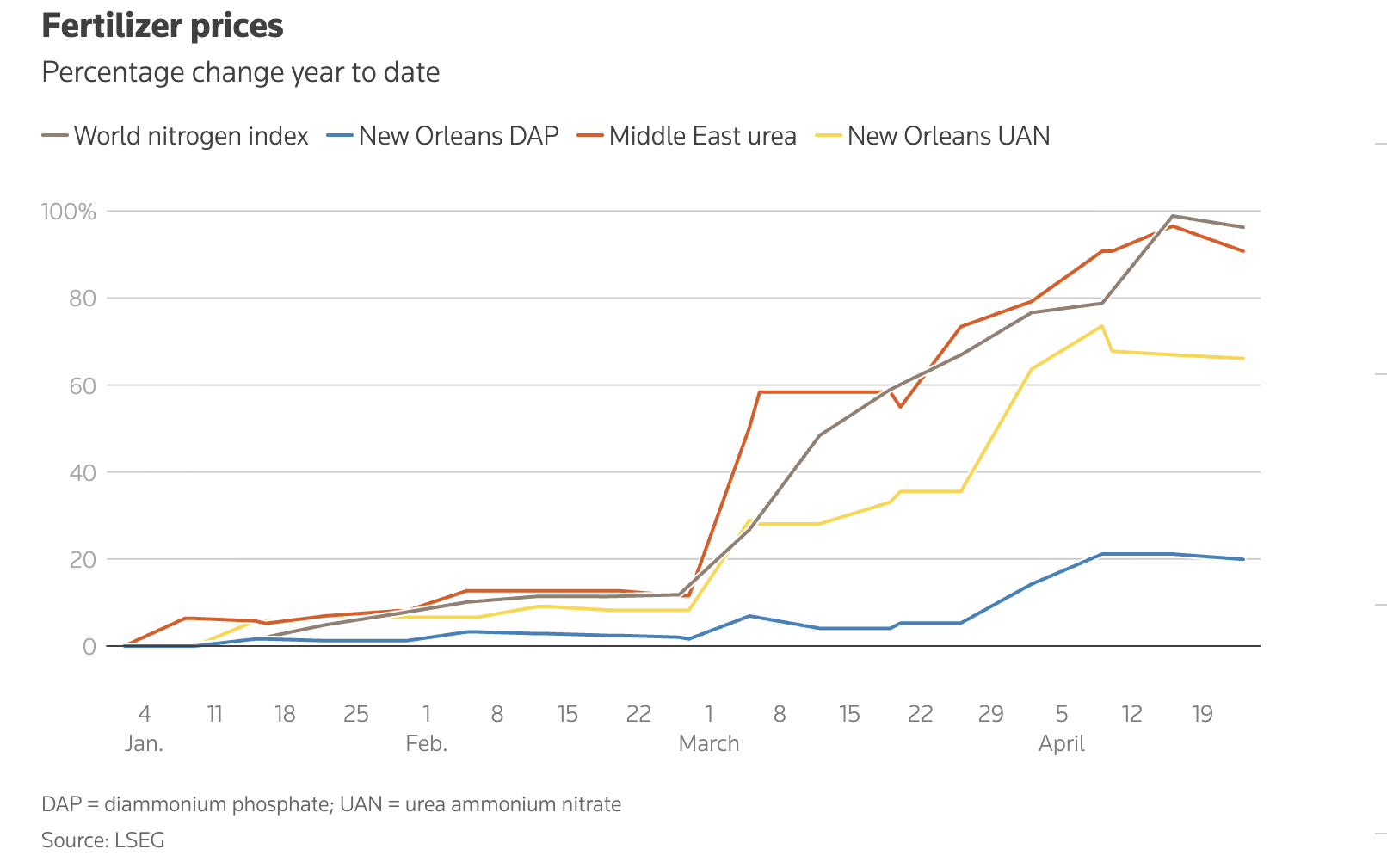

A growing global food crisis is unfolding right now as the war in Iran disrupts fertilizer shipments and cripples rice production across Asia, threatening one of the world’s most essential food supplies.

Farmers across multiple major rice-producing nations are being forced to cut back on planting and reduce their expected harvests as soaring fuel and fertilizer costs spread through already fragile supply chains. Experts warn the shockwaves from these reductions could soon impact grocery prices and food availability worldwide.

The critical wet-season rice planting window for much of South and Southeast Asia runs from May to August. This is the period when farmers decide how much land to plant and how much fertilizer to apply. Multiple independent reports from the past few weeks confirm that many farmers are now scaling back or skipping planting altogether.

Reuters reported on April 30, 2026, that the rice supply is expected to fall as farmers across Asia cut planting acreage due to soaring fertilizer and fuel costs. Nikkei Asia on May 6, 2026, and the Washington Post on May 9, 2026, both confirmed that farmers in Thailand, Vietnam, India, Bangladesh, the Philippines, and Indonesia are leaving fields idle or deciding not to plant the next crop because production costs have become unprofitable.

From Reuters (April 30, 2026):

“Rice supply is expected to fall this year as farmers cut planting acreage across Asia because of fertiliser shortages and soaring fuel costs from the Iran war, with an emerging El Niño also set to squeeze output of the world’s most consumed staple,” Reuters reported. In Thailand’s Chai Nat province, 60-year-old farmer Sripai Kaew-Eam told Reuters that high fertiliser and fuel prices have pushed production costs to about 6,000 baht ($183.99) per rai (0.4 acre), up from 4,500–5,000 baht for the previous crop. Fertiliser prices have risen to 1,000–1,200 baht per bag from 850 baht, forcing her to cut her use by half.

Nikkei Asia reported on May 6, 2026 that rice farmers in India, Vietnam, and Thailand are bracing for a severe fertilizer shock as the growing season begins. The World Bank forecasts that overall fertilizer prices will rise 31% in 2026 compared with 2025, with urea — the most widely used nitrogen fertilizer — potentially climbing by as much as 60%. “Soaring fertilizer prices are looming over rice farmers in South and Southeast Asia as they prepare for the growing season, posing a risk to the food supply,” the article noted, highlighting how the Strait of Hormuz crisis is driving up the cost of essential inputs at the worst possible time.

The The Washington Post (May 9, 2026) that the Iran war is “crushing Asia’s farmers” and threatening global food supply. The article detailed how farmers across the region are making irreversible cuts as they enter key planting seasons, with the combined impact of higher diesel and fertilizer costs forcing many to leave fields idle or dramatically reduce inputs.

“Rising fuel and fertilizer costs led Saithong Jamjai to stop cultivating rice and shift to fruit crops on her farm in Nonthaburi, Thailand,” Because of surging prices driven by the war, planting and harvesting will cost her at least $33,000, she said.

Analysts estimate this could lead to a 10–15% reduction in rice output in the affected regions for the coming harvest, with the most significant effects being felt from October–November 2026 onward.

This is not speculation. It is happening in real time as farmers make their planting decisions during the key growing window.

We have been warning about the coming famine since 2005 using the Sabbatical and Jubilee cycles as our guide. What we are seeing now matches exactly the pattern of curses that Yehovah warned Israel about in Leviticus 26:

“I will break the pride of your power; and I will make your heaven as iron, and your earth as brass: And your strength shall be spent in vain: for your land shall not yield her increase, neither shall the trees of the land yield their fruits.” (Leviticus 26:19-20)

“When I have broken the staff of your bread, ten women shall bake your bread in one oven, and they shall deliver you your bread again by weight: and you shall eat, and not be satisfied.” (Leviticus 26:26)

These verses describe a time when the land refuses to produce its full increase and food becomes so scarce that even basic baking requires extreme effort and rationing.

The war in Iran has now triggered the very mechanisms that can produce this kind of famine: disrupted fertilizer shipments from the Persian Gulf, skyrocketing fuel prices, and farmers in Asia being forced to plant less rice. The systems we depend on for food are reaching their limits.

Sources:

Reuters, April 30, 2026 – Rice supply expected to fall as farmers cut planting due to fertilizer and fuel costs.

Nikkei Asia, May 6, 2026 – Reports on fertilizer shock and reduced planting in Thailand, Vietnam, and India.

Washington Post, May 9, 2026 – Farmers in Asia scaling back rice planting due to surging costs.

Here is the full article from which we draw some of our abbreviated piece above.

A worker cultivates rice plants at a farm in Bangkok, Thailand, August 28, 2018. Picture taken August 28, 2018. REUTERS/Soe Zeya Tun/File Photo Purchase Licensing Rights, opens new tab

Summary

Higher fertiliser, fuel costs prompt rice farmers to cut inputs

Growers in key producing countries cut rice planting

Dryness due to El Nino weather to further strain grain supplies

Situation getting “pretty serious” if fertiliser remains blocked

SINGAPORE/BANGKOK, April 30 (Reuters) – Rice supply is expected to fall this year as farmers cut planting acreage across Asia because of fertiliser shortages and soaring fuel costs from the Iran war, with an emerging El Nino also set to squeeze output of the world’s most consumed staple.

Rice is central to global food security, and even modest supply disruptions can ripple through countries, lifting prices and straining household budgets, particularly among price-sensitive consumers in Asia and Africa. The UN Food and Agriculture Organization in April forecast rice output would expand by 2% to a record high in 2025/26.

The Reuters Iran Briefing newsletter keeps you informed with the latest developments and analysis of the Iran war. Sign up here.

Advertisement · Scroll to continue

” />

The effects of the Iran war are impacting farmers in top exporters Thailand and Vietnam as well as the import-reliant Philippines and Indonesia, growers and traders said. The war has cut fuel and fertiliser flows through the Strait of Hormuz, a key chokepoint that connects the Gulf to global markets.

Southeast Asia’s mainly smallholder farmers also face mounting stress as the El Nino weather phenomenon is set to usher in hotter, drier conditions for the region in the second half of the year.

“Farmers have already started planting rice in some countries and are using fewer inputs because prices have gone up,” said Maximo Torero, chief economist at the UN FAO. “We are going to see a tighter global supply situation in the second half of the year and early next year.”

In 2008, export curbs by key suppliers more than doubled prices to about $1,000 a metric ton , triggering unrest in several countries. More recently, supply tightness in 2022 to 2023, exacerbated by India’s export restrictions, lifted prices and prompted panic buying.

SUPPLY-CHAIN DISRUPTION

Rice shipments are already facing supply-chain bottlenecks.

“Logistics have become a nightmare, especially in Asia as there is shortage of polypropylene bags, limited truck availability to move rice to ports and shipping itself has been disrupted,” said a Singapore-based trader at a top global rice merchant, who asked to remain unidentified as they are not authorized to speak to media.

While fertiliser shortages and dryness are already curbing yields of smaller crops being harvested in Southeast Asia, the next crop will likely face a bigger reduction.

India, Thailand and the Philippines plant their main crops in June and July, while Vietnam and Indonesia are now sowing their second-season crops.

Most Asian producers grow two or three rice crops a year.

FARMERS CUT PLANTING

Sripai Kaew-Eam, a 60-year-old farmer in Thailand’s Chai Nat province about 151 km (94 miles) north of Bangkok, said high fertiliser and fuel prices have pushed production costs to about 6,000 baht ($183.99) per rai (0.4 acre), from around 4,500 to 5,000 baht for the previous crop, while the price she receives for the unhusked rice she harvests is about 6,200 baht per metric ton.

Fertiliser prices have risen to 1,000 to 1,200 baht per bag, from 850 baht, forcing her to cut her use by half.

“Fertiliser prices are high, fuel prices are high,” she said.

The Philippines, the world’s biggest rice importer, faces a similar situation.

“Some farmers are now saying they may not plant or will reduce fertiliser use, which would inevitably cut production,” said Arze Glipo, executive director of the Integrated Rural Development Foundation.

The country’s output could fall by as much as 6 million tons from its typical 19 million to 20 million.

“That would leave the Philippines in a precarious position, as imports are also uncertain due to export restrictions, making it extremely difficult to cover any production shortfall,” Glipo said.

In Indonesia, fertiliser supply is not a constraint but the El Nino is expected to curb output.

Indonesia’s statistics bureau estimates the rice harvest area in the March to May period will shrink by 10.6% to 3.85 million hectares (9.5 million acres), while unhusked rice production will drop 11.12% to 20.68 million tons.

Despite the supply worries, the world has ample rice inventories following years of bumper output, with India, the world’s biggest exporter, holding a record 42 million tons or about one-fifth of global stockpiles, according to U.S. Department of Agriculture data, cushioning any drop in global production.

Most rice grade prices are currently steady but will likely rise even if the Hormuz situation were resolved immediately, the FAO’s Torero said.

Opening the strait soon would avoid a major supply issue but “if we don’t reopen this in the next two to three weeks, the situation is going to get pretty serious,” he said.

($1 = 32.61 baht)

Reporting by Naveen Thukral in Singapore and Panarat Thepgumpanat in Bangkok; additional reporting by Karen Lema in Manila, Bernadette Christina in Jakarta, Khanh Vu in Hanoi and Mayank Bhardwaj in New Delhi; Editing by Christian Schmollinger

Winter Wheat Condition & Spring Wheat Planting Progress & Global Wheat Report(as of May 3, 2026)

Winter Wheat Condition & Spring Wheat Planting Progress & Global Wheat Report (as of May 3, 2026)

Here is the most up-to-date information (as of May 10, 2026) on the U.S. drought situation, including winter wheat, spring wheat planting progress, and the global wheat market impact.

Winter Wheat Condition (as of May 3, 2026)

The winter wheat crop remains in very poor shape across the Southern and Central Plains.

Good to Excellent: 31% (well below the 5-year average and sharply worse than last year).

Poor to Very Poor: 37% (up significantly from last year).

The hardest-hit states are Kansas, Oklahoma, Texas, Colorado, and Nebraska, where drought coverage remains extreme.

Spring Wheat Planting Progress (as of May 3, 2026)

Spring wheat planting in the top six producing states is lagging behind normal:

Planted: 32% (10 points behind last year’s 42% pace and 3 points behind the 5-year average of 35%).

Emerged: 10% (slightly ahead of the 5-year average of 9%).

Washington is leading at 87% planted, while North Dakota is lagging at only 19% planted.

Source: Same USDA Crop Progress Report (May 4, 2026) above.

Global Wheat Market Impact

The severe U.S. drought is already pushing global wheat prices higher:

Chicago wheat futures have gained nearly 30% since the start of 2026, reaching levels not seen in almost two years.

Analysts estimate total U.S. wheat production for 2026 could be down ~15% from 2025 levels due to reduced planted acres, high abandonment rates in the Southern Plains, and lower yields.

The U.S. is one of the world’s largest wheat exporters. Reduced U.S. output, combined with fertilizer shortages affecting Asian rice and other crops, is tightening global supplies and supporting higher prices worldwide.

The U.S. drought continues to severely damage the 2026 winter wheat crop, with spring wheat planting also running behind normal pace. This is contributing to a meaningful tightening of global wheat supplies and higher prices heading into the 2026/27 marketing year.

The situation remains fluid. The next USDA Crop Progress report (for the week ending May 10) will be released on Monday, May 11, 2026.

Global Wheat Report – Major Producing Countries (as of May 10, 2026)Here is a concise, up-to-date overview of the world’s top wheat-producing countries, focusing on the 2026 harvest (mostly Northern Hemisphere winter and spring wheat being harvested June–August 2026) and planting intentions for the next cycle (fall 2026 / 2026-27 crop).1. United States (Major exporter)

2026 Harvest: Very poor. Winter wheat condition is among the worst in recent memory due to severe drought in the Southern and Central Plains. Good-to-excellent rating only 31%, poor-to-very-poor 37%. Production expected down ~15% from 2025.

Spring wheat planting (as of early May 2026): Lagging at 32% planted (behind last year and 5-year average).

Planting for 2026-27: All-wheat planted area estimated at 43.8 million acres, down 3% from 2025 and the lowest since records began in 1919.

2. European Union (Major exporter)

2026 Harvest: Slightly lower overall. Yields mixed; some countries (Germany, Italy) down, others (Bulgaria, Poland, Spain) better. Total EU production expected modestly lower than the 2025 record.

Planting for next cycle: Not yet fully reported, but high input costs and low prices are expected to reduce acreage in 2026-27.

3. China (Largest producer, mostly domestic use)

2026 Harvest: Stable to slightly higher. Large domestic stocks cushion any minor fluctuations.

Planting for next cycle: Generally stable; China maintains high domestic production priority.

4. India (Large producer and occasional exporter)

2026 Harvest: Record or near-record levels due to strong sowings and favorable weather in key regions.

Planting for next cycle: Expected to remain high as government supports domestic food security.

5. Russia (Top global exporter)

2026 Harvest: Slightly lower than the previous record due to reduced planted area, though yields remain solid in many regions.

Planting for next cycle: Lower acreage expected due to profitability concerns and shifting crop mixes.

6. Canada (Major exporter)

2026 Harvest: Spring wheat planting lagging; overall production expected lower than 2025.

Planting for 2026-27: Acreage projected to decline as farmers shift to more profitable oilseeds.

7. Australia (Major Southern Hemisphere exporter)

2026 Harvest (just finished or finishing): Lower than the strong 2025 crop due to drier conditions in some areas.

Planting for next cycle (April–June 2026): Expected to be lower due to weather uncertainty and input costs.

8. Ukraine (Significant exporter despite war)

2026 Harvest: Lower than pre-war levels but relatively stable year-over-year; some yield improvements offset reduced area.

Planting for next cycle: Limited data, but logistical and conflict-related challenges continue to constrain full recovery.

Global Summary

2026 Harvest (current season): Mixed. Record or near-record global production in 2025/26 (around 844 million metric tons), but the 2026 Northern Hemisphere crop is weaker in key exporters (U.S., Russia, Canada, Australia) due to drought, lower acreage, and higher input costs.

Planting for 2026-27: Global wheat acreage is trending lower in most major producers. Farmers are shifting to more profitable crops (soybeans, corn, oilseeds) because of low wheat prices and high fertilizer/fuel costs. The International Grains Council (IGC) and USDA project a decline in global wheat production for 2026/27 compared with the 2025/26 record.

Bottom line: The current 2026 harvest is disappointing in several key exporting countries (especially the U.S.), while planting intentions for the next season are contracting worldwide. This tightening of supply is already supporting higher wheat prices and will likely contribute to upward pressure on global food costs later in 2026 and into 2027.

Current Global Surplus Food Stocks

Current Global Surplus Food Stocks

There is a significant risk of food shortages and sharp price increases in 2026 and especially in 2027, driven by the combined pressures of the U.S. drought, reduced Asian rice planting, the Iran war’s impact on fuel and fertilizer costs, and a developing El Niño.

Current Global Surplus Stocks (Buffer to Absorb a Shock)

Global grain stocks are currently at record or near-record levels, providing a temporary cushion:

Wheat: Global ending stocks for the 2025/26 season are forecast at 283.1 million tonnes (a 5-year high). This represents a comfortable stocks-to-use ratio of around 32–34%.

Rice: Global ending stocks for 2025/26 are projected at 191–192 million tonnes (also near record highs), enough to cover about 4.7 months of world consumption.

Sources:

USDA/IGC April–May 2026 reports

FAO Cereal Supply and Demand Brief (May 2026)

These stocks give the world some breathing room for one moderate shock. However, the current multi-front crisis (U.S. drought + Asian rice planting cuts + fertilizer/fuel cost spike + El Niño) is not a single shock — it is a compounding, multi-year disruption. Stocks can be drawn down quickly if production shortfalls persist into 2026/27.

Projected Shortfalls and Timeline for Shortages

2026 (current harvest year): Wheat production in key exporters (U.S., Russia, Canada, Australia) is already lower due to drought and reduced planting. Rice output in Asia will be noticeably reduced because of current planting cuts (May–August 2026 window). Prices will rise, and localized shortages will appear, especially in import-dependent regions. No global famine, but significant tightening.

2027: The full impact of lower 2026 planting + El Niño effects on the 2026/27 harvest will hit hardest. Global wheat and rice supplies are forecast to decline further. This is when widespread shortages, rationing in some countries, and major price spikes become most likely.

Analysts (IGC, FAO, USDA) project global wheat production to drop 2–5% in 2026/27 and rice output in Asia to fall 10–15% in key producing regions due to the fertilizer/fuel crisis. Combined with El Niño, this creates a multi-year supply squeeze.

Most Vulnerable Nations

The countries most at risk are those that are:

Highly dependent on wheat and rice imports, and

Already facing conflict, poverty, or climate stress.

Top vulnerable nations (2026–2027):

Bangladesh, Philippines, Indonesia, Nigeria — heavy rice importers with large populations and limited domestic buffers.

Egypt, Yemen, Sudan, Lebanon — major wheat importers already under strain.

East Africa (Ethiopia, Kenya, Somalia) and Sahel countries — compounded by drought and conflict.

Pakistan and India (internal shortages possible if domestic production falls sharply).

The 2026 Global Report on Food Crises already projects 266–318 million people facing acute hunger in 2026, with risks rising sharply into 2027 if grain supplies tighten further.

Bottom line: We currently have enough stocks to absorb a single-year moderate shock, but not a sustained multi-year disruption across both wheat and rice. The 2026–2027 period is when the real pressure will build. Shortages will likely appear first as higher prices and empty shelves for staples, then as more severe access problems in vulnerable countries.

This situation aligns precisely with the warnings in Leviticus 26 about the land refusing to yield its increase when a nation turns away from God’s commandments.

Sources (all verified May 2026):

USDA/IGC Grain Market Reports (April–May 2026)

FAO Cereal Supply and Demand Brief (May 2026)

Reuters, Nikkei Asia, Washington Post reporting on Asian rice planting (April–May 2026)

• • Global Report on Food Crises 2026

14 Comments

Gary

on 15/05/2026 at 7:17 am

Shalom Joe

Can I ask you a question?

In revelation 17:17

Rev 17:17 For God put it in their hearts to do what will fulfill his purpose, that is, to be of one mind and give their kingdom to the beast until God’s words have accomplished their intent.

I want to ask could the powers of the world be doing some of the things you just brushed aside but still fulfilling Gods plan ?

Like it’s easy to say God is doing everything and I’m in full agreement with you and I know you have been sharing so much for so long, what comes to mind is this, when God sent the kingdom of the North to chastise Israel He used people to achieve this right ? So why can’t the people interfering with the weather and other things be apart of Gods plan?

Honestly I truly believe you can do damage to those little lambs who’ve woke up to the evils of this world, but then humiliating them in your actions by just dismissing everything they’ve come to know.

I pray this finds you well and you hear I’m not trying to beat anyone down etc just an observation I’ve seen for quite some time…

Have a blessed sabbath rest and much love in Yeshua Messiah to you Joe and all the body

Shalom Gary, thanks for the comments. As you know since 2005, I have been putting this message out. And all of those who want to dismiss it and ignore it and laugh at it are those same people who cling to the HAARP and chem trail lunacies amongst others. They have turned the Torah into a conspiracy camp of fools. In the news right now are “believers bringing in the newest UFO teachings.

All of it is idolatry and the mixing of Torah with false teachings. It is no different, none at all, no different than mixing in Christmas and Easter with the Torah and justifying it because it brings families together.

I am, and have been making it painfully clear, it is Yehovah who sends the Tornadoes, Hurricanes, Typhoons, droughts, floods, and catastrophes. Not Bill Gates or George Soros. But Yehovah and Him alone. And if people would stop all their nonsense they might just see that and understand just how mad He is and how close the end truly is. But they don’t because it is Global warming and just another natural cycle and has nothing to do with God. It is normal. If my calling people out is upsetting then as you already know, I am not about to stop doing it and have done so for the past 21 years.

Those little lambs you speak about, have grown into old tough ewes and rams with intrenched conspiracy torah mixtures. The cull that is coming will remove many who continue to mix the truth with lies. They need to spend their time studying Torah and less time becoming experts about chemtrails and the Nehphelim. In 21 years my message has not changed one iota on this. Lets teach those little lambs Torah and stop teaching them nonsense that will not be of any use in the 7th millennium kingdom just 18 years from now.

Here is something to think about which Amit Segal just wrote.

George Orwell once said, “Some ideas are so stupid that only intellectuals believe them.”

Give my regards to your family and in-laws.

Shabbat Shalom

Thank you for your reply Joe, very much appreciate your time. Thank you for your kind regards to my family and I and my family in the Philippines 🇵🇭

An in person conversation would probably be best for this topic as communication is key.

First off as I’ve said in my first email, I’m in full agreement that YHVH Elohim is in complete control of everything.

The little lambs are ones who woke up to the darkness, just like a seed, it doesn’t wake up with the light ( truth ) but in darkness and then seeks the light… we don’t cut off our root system that woke up to the devils lies ( he is the father of lies ) and has pulled the wool over all our eyes in many things.

I don’t preach any of this as I’ve been led to the Torah and strive to walk uprightly in the truth by His Spirit ( some good days some bad )

So what im trying to get across is this – if God used the kingdom of the north to chastise Israel, one could say God did that and the answer is yes but also someone can say the kingdom of the north chastised Isreal and they too would be correct. So if God uses people to achieve His cause to negate this simple fact would be error and brushing aside someone who woke up to many lies to just say that doesn’t exist may be detrimental to someone’s walk. We must meet everyone where they’re at on an individual basis because that’s the picture of a home, a father has many different aged children and he must address each one individually and help grow them in their walk.

We see God allowing Satan to buffet Job and we know it’s ultimately Gods work but Satan buffeted and just maybe the same is happening in certain situations here on earth now.

Joe I live in Ireland and we get very little sunshine at times and when we do they spray the sky ( I don’t know what with ) but it is happening. To say it doesn’t isn’t happening would be a lie.

I hope you hear what point im trying to make, I’m not saying preach all about them but to acknowledge there is a sinister people who are not for you or I and they have shady things happening all over the world.

So could God use people to achieve His goal, my answer is a resounding yes, all one must do is read the Word and see He always did use people. Just like the vine and the branches ( the branches produce the fruit but it’s Yah ultimately giving His power )

I hope all that makes sense…

I hope and pray I don’t come across as arrogant or prideful etc or argumentative, it’s surely not my intention. I reckoned I read your articles every week and yeshua was asked many questions so I thought I should also and not sit here in Ireland wondering should I or shouldn’t I but just do it.

Shalom and blessings be upon you and your ministry I pray

I lean to your explanation Gary. God always uses man and nations as tools of judgement. Then we have the Tower of Babel where mankind wanted to ascend to heaven and become as God.

Modern technology and AI is allowed us to become as God.

In some respects He will leave us to our own devices.

It is entirely possible there is some technology being used to create weather.

Even so it is still Yah allowing man to ascend and be judged.

We will ultimately be held responsible for the judgment coming.

Shalom brothers. I am compelled to point out how mankind has failed at his job, the ruler of this earth (mankind, Ge 1:28) is falling on his face. Such irony! Here as Josephs points out, we may be headed towards unprecedented drought, and the same ‘geniuses’ who think they can solve ‘climate change’ (lol, yeah, duh climate changes) all of a sudden have forgotten about their long established religion and no longer preach reducing CO2 because they need rediculous amounts of energy to animate their AI god, which is being created in mankinds image, which also needs much water to keep the data centers cooled. So, our great geniuses, the greatest minds of the world, are using the very resources that mankind itself needs to survive to animate their god. Only Yehovah Himself can deliver us from ourselves.

Yes, Yah is angry but conspiracy is real. Man is a rebellious tool of haSATAN. Our technology is being used against us.

HaSatan is a conspiratorial beast and because we are turning away from Jehovah he is being allowed to be part of the judgement.

The Bible is full of stories where God uses man or nations as tools of His judgement or blessings. King Jehu was used to rid Israel of King Ahab and Jezebel is one example.

The World Economic Forum is a conspiracy to rule the world…yah is laughing at them, but they are a tool of His judgement and because the world a large is turning away from the creator they become a tool of judgement.

In the end Yeshuah will come and save us.

Just want to make myself clear, Yehovah is clearly the Author of the curses and “climate change”. It is in the wake of Yehovah’s curses, mankind is oblivious and working against Him, trying to snake his way around the curses Yehovah is bringing. Are we ‘waging war’ against our Creator?

As I shared in my two posts, I am in full agreement that it is YHVH who is punishing His creation and it’s His Will being done upon the Earth.

To simplify my point I’m trying to make is this — if I go fishing and I catch a fish, it’s me who caught it, but I used a fishing pole. So to say there was no fishing pole is obviously false.

The fishing pole is the people of this world who think they run it. Our Heavenly Father is and always will be in control and even if they think they’re going against Him, they are not because as Neil pointed out Yah is laughing at them and using them to achieve His will.

Thanks Gary and Neil, you are correct. Also Yah created all of us and we have no right tocall others fools and stupid. Yah and hasatan use people. This site warns us to store up some food for the future to get us by. I will quote 1st Kings 17: 2 – 6. The crows fed Elijiah twice a day…sounds a little contrdictory dont it. Most believe what we were taught example : the globe theory and flat earth. Which one is conspiracy? Why call some one out on it from eather side. It is what it is ! Our mindset should be does it matter to us at the end of time. What matters most is obediance! Thus we must be obediant and reach out to the lost to give them the warmth and watering of the word that the little seed will sprout. I pray this site will be a little more mindful of that rather than conspiracy and political.

Gary you have said it well.

While it is true that YHVH is the one who sends these calamities on us to hopefully bring us to repentance for our sins it is also true that there are men in those planes leaving streaks across our skies. Someone paid for the fuel and the payload to be dumped.

What we see with our own eyes is real. To deny it is delusional. To ridicule and shame those who acknowledge what they see is discrediting at least. Abusive even.

There are many names for the activity in the sky Geoengineering is one. Look it up. It’s come along way from its beginning.

It is because of my interest in the “conspiracy theory” that yhvh used to get me to listen to him. To try it his way.

Now after years of being told to focus on Torah only and bible only and being shamed and treated poorly for continuing to delve into these so called conspiracies that I have to come to realize the depth of the deception that YHVH has been trying to open my eyes to.

The whole world has been deceived. It is past tense not some event to come at the end. You have been deceived. Acknowledge it and maybe you can come out of her.

Im not writing to be the one to pry open your eyes with a pry bar. I want to see those who see this world for what it is treated with respect. We are not stupid as some would say.

Deception is like a diamond having many facets. It is not possible to see all of them at one time they are part of the same thing sharing the same root purpose and end goal. To keep you from getting a good clear view of

reality. To keep us in a state of division.

Understanding the world and wanting to share it should not have to separate us from the body of yeshua.

When you can’t argue the facts attack the character is a tactic used to control the conversation. Speak to the facts.

And the fact is that we have all been deceived. How much is the question.

Come out of her my people is about this. Open your eyes to the world around you be fore you are so wrapped up in it you can’t accept a challenge to your current understanding.

Satan exists and is working to deceive you accept it and be on the look out. Do you really think you are smart enough to say Iam not deceived. This would be delusion.

Know your enemy is a good tactic in battle. Physical and spiritual.

Keep your eyes peeled.

Shalom

Kurt

Without negating Mr. Dumond’s YHVH-sent wisdom, I see the other 7 published comments above as also valid and basically-balanced modifications.

I’ll add this: Y’shua urged/ordered the traitor Judas to “go quickly” as Satan’s tool… thus fulfilling YHVH’s ultimate goal of the unjust crucifixion. Without that ‘tool of satan’ human history would be unsave-able and damned. So should we ironically thank Satan’s scriptural naivety?… .just askin’ for a friend!

For 21 years now I have shown the curses of Yehovah only to be beaten down by brethren claiming it was HAARP, chemtrails, or something else. They ignored Yehovah’s hand and focused instead on the “fishing rod” — the conspiracy itself. I rebuked them then, and I rebuke them now.

I don’t give a damn about the fishing rod, the line, the lure, or the spinner. I am focused on Yehovah and His movements and His actions alone.

Many people have thanked me over the years for exposing the fallacies of the conspiracies they had fallen into. Once they stopped diving into that witchcraft, they finally understood how deceived they had been. Yet even though they have never proven the earth is flat, or the claims about HAARP, or any of the other theories they promote, they still refuse to repent. They continue believing and teaching these false ideas, mixing them with the Torah instead of teaching Yehovah and Him alone.

When a new person hears someone speaking about Yehovah and then immediately launching into chemtrails, HAARP, Flat Earth, Nephilim fantasies, Sovereign citizens or secret cabals trying to kill us all, what happens?

If they are smart, they run.

They see the Torah of Yehovah being bastardized and mixed with crazy, hallucinative teachings. Instead of pure truth, they hear a toxic blend of Scripture and conspiracy rabbit holes. The result? The Name of Yehovah gets associated with foolishness, and the newcomer flees — often never to return.

Many would not take part in our midrashes because someone wanted to talk about some conspiracy.

This is exactly what Scripture warns against.

God says in Jeremiah 4:22:

For My people are foolish; they have not known Me; they are stupid sons, and they have no understanding. They are wise to do evil, but to do good they have no knowledge. MKJV

And in Proverbs 12:1:

Pro 12:1 Whoever loves discipline loves knowledge, But he who hates reproof is stupid. TS 2009

Yehshua echoed the same:

Mat 23:17 Fools and blind! For which is greater, the gold, or the temple that sanctifies the gold?

Mat 23:18 And, Whoever shall swear by the altar, it is nothing; but whoever swears by the gift that is on it, he is a debtor!

Mat 23:19 Fools and blind! For which is greater, the gift, or the altar that sanctifies the gift?

Luk 24:25 And He said to them, O fools and slow of heart to believe all things that the prophets spoke!

Those who refuse correction, who endlessly dive into the next wild theory and mix it with Torah, are doing precisely this. They drive people away from the pure Word of Yehovah. They make the Torah look crazy instead of holy.

New seekers come looking for the God of Abraham, Isaac, and Jacob — for His Sabbaths, His Appointed Times, and His commandments. Instead, they get flooded with fear-porn and unprovable fantasies.

Repent.

Stop bastardizing the Torah with your crazy talk. Come out of the rabbit holes. Return to the clean, uncorrupted teaching of Yehovah’s Word.

If you keep mixing these things, the smart ones will keep running — and Yehovah will continue to call your behavior what it is: stupid.

Choose wisdom. Teach pure Torah. Leave the conspiracies behind. Yehovah gives clear, repeated commands against adding to, subtracting from, or mixing His Torah with other teachings, traditions, or practices. This includes blending it with foreign ideas, conspiracies, or human inventions.

Core Commands Against Adding or Mixing:

* Deuteronomy 4:2 (MKJV or similar literal) “You shall not add to the word which I command you, nor take from it, that you may keep the commandments of Yehovah your God which I command you.”

* Deuteronomy 12:32 “Whatever I command you, be careful to observe it; you shall not add to it nor take away from it.”

* Proverbs 30:6 “Do not add to His words, lest He rebuke you, and you be found a liar.”

These verses directly forbid mixing extra teachings (like conspiracies, extra “revelations,” or pagan-influenced ideas) with the pure Torah. Adding to it corrupts obedience.

Warnings Against Mixing Worship and Practices (Syncretism):

* Deuteronomy 12:4, 29-31 “You shall not worship Yehovah your God in that way [the way the nations worship their gods]… Take heed… that you do not inquire after their gods, saying, ‘How did these nations serve their gods? I also will do likewise.’ You shall not worship Yehovah your God in that way; for every abomination to Yehovah which He hates they have done to their gods.”

* Deuteronomy 12:30-32 (summary) Do not learn the ways of the nations and mix them into your worship of Yehovah. Do exactly what He commands — nothing more, nothing less.

* Jeremiah 10:2 “Do not learn the way of the Gentiles…”

Yehovah repeatedly warns Israel against blending His holy Torah with the customs, fears, or wisdom of the surrounding world. Mixing creates a “toxic blend” that profanes His Name and drives people away.

These commands apply today: Teach Yehovah and His Torah alone — pure and uncorrupted. Do not mix in chemtrails, HAARP, Flat Earth, Nephilim obsessions, or any other rabbit-hole teachings. To do so is to add to His Word and disobey these clear scriptures.

Repent and return to the pure Torah of Yehovah.

Shalom Joe

Can I ask you a question?

In revelation 17:17

Rev 17:17 For God put it in their hearts to do what will fulfill his purpose, that is, to be of one mind and give their kingdom to the beast until God’s words have accomplished their intent.

I want to ask could the powers of the world be doing some of the things you just brushed aside but still fulfilling Gods plan ?

Like it’s easy to say God is doing everything and I’m in full agreement with you and I know you have been sharing so much for so long, what comes to mind is this, when God sent the kingdom of the North to chastise Israel He used people to achieve this right ? So why can’t the people interfering with the weather and other things be apart of Gods plan?

Honestly I truly believe you can do damage to those little lambs who’ve woke up to the evils of this world, but then humiliating them in your actions by just dismissing everything they’ve come to know.

I pray this finds you well and you hear I’m not trying to beat anyone down etc just an observation I’ve seen for quite some time…

Have a blessed sabbath rest and much love in Yeshua Messiah to you Joe and all the body

Shalom

Shalom Gary, thanks for the comments. As you know since 2005, I have been putting this message out. And all of those who want to dismiss it and ignore it and laugh at it are those same people who cling to the HAARP and chem trail lunacies amongst others. They have turned the Torah into a conspiracy camp of fools. In the news right now are “believers bringing in the newest UFO teachings.

All of it is idolatry and the mixing of Torah with false teachings. It is no different, none at all, no different than mixing in Christmas and Easter with the Torah and justifying it because it brings families together.

I am, and have been making it painfully clear, it is Yehovah who sends the Tornadoes, Hurricanes, Typhoons, droughts, floods, and catastrophes. Not Bill Gates or George Soros. But Yehovah and Him alone. And if people would stop all their nonsense they might just see that and understand just how mad He is and how close the end truly is. But they don’t because it is Global warming and just another natural cycle and has nothing to do with God. It is normal. If my calling people out is upsetting then as you already know, I am not about to stop doing it and have done so for the past 21 years.

Those little lambs you speak about, have grown into old tough ewes and rams with intrenched conspiracy torah mixtures. The cull that is coming will remove many who continue to mix the truth with lies. They need to spend their time studying Torah and less time becoming experts about chemtrails and the Nehphelim. In 21 years my message has not changed one iota on this. Lets teach those little lambs Torah and stop teaching them nonsense that will not be of any use in the 7th millennium kingdom just 18 years from now.

Here is something to think about which Amit Segal just wrote.

George Orwell once said, “Some ideas are so stupid that only intellectuals believe them.”

Give my regards to your family and in-laws.

Shabbat Shalom

Thank you for your reply Joe, very much appreciate your time. Thank you for your kind regards to my family and I and my family in the Philippines 🇵🇭

An in person conversation would probably be best for this topic as communication is key.

First off as I’ve said in my first email, I’m in full agreement that YHVH Elohim is in complete control of everything.

The little lambs are ones who woke up to the darkness, just like a seed, it doesn’t wake up with the light ( truth ) but in darkness and then seeks the light… we don’t cut off our root system that woke up to the devils lies ( he is the father of lies ) and has pulled the wool over all our eyes in many things.

I don’t preach any of this as I’ve been led to the Torah and strive to walk uprightly in the truth by His Spirit ( some good days some bad )

So what im trying to get across is this – if God used the kingdom of the north to chastise Israel, one could say God did that and the answer is yes but also someone can say the kingdom of the north chastised Isreal and they too would be correct. So if God uses people to achieve His cause to negate this simple fact would be error and brushing aside someone who woke up to many lies to just say that doesn’t exist may be detrimental to someone’s walk. We must meet everyone where they’re at on an individual basis because that’s the picture of a home, a father has many different aged children and he must address each one individually and help grow them in their walk.

We see God allowing Satan to buffet Job and we know it’s ultimately Gods work but Satan buffeted and just maybe the same is happening in certain situations here on earth now.

Joe I live in Ireland and we get very little sunshine at times and when we do they spray the sky ( I don’t know what with ) but it is happening. To say it doesn’t isn’t happening would be a lie.

I hope you hear what point im trying to make, I’m not saying preach all about them but to acknowledge there is a sinister people who are not for you or I and they have shady things happening all over the world.

So could God use people to achieve His goal, my answer is a resounding yes, all one must do is read the Word and see He always did use people. Just like the vine and the branches ( the branches produce the fruit but it’s Yah ultimately giving His power )

I hope all that makes sense…

I hope and pray I don’t come across as arrogant or prideful etc or argumentative, it’s surely not my intention. I reckoned I read your articles every week and yeshua was asked many questions so I thought I should also and not sit here in Ireland wondering should I or shouldn’t I but just do it.

Shalom and blessings be upon you and your ministry I pray

I lean to your explanation Gary. God always uses man and nations as tools of judgement. Then we have the Tower of Babel where mankind wanted to ascend to heaven and become as God.

Modern technology and AI is allowed us to become as God.

In some respects He will leave us to our own devices.

It is entirely possible there is some technology being used to create weather.

Even so it is still Yah allowing man to ascend and be judged.

We will ultimately be held responsible for the judgment coming.

Shalom brothers. I am compelled to point out how mankind has failed at his job, the ruler of this earth (mankind, Ge 1:28) is falling on his face. Such irony! Here as Josephs points out, we may be headed towards unprecedented drought, and the same ‘geniuses’ who think they can solve ‘climate change’ (lol, yeah, duh climate changes) all of a sudden have forgotten about their long established religion and no longer preach reducing CO2 because they need rediculous amounts of energy to animate their AI god, which is being created in mankinds image, which also needs much water to keep the data centers cooled. So, our great geniuses, the greatest minds of the world, are using the very resources that mankind itself needs to survive to animate their god. Only Yehovah Himself can deliver us from ourselves.

I would not want to be accused of giving ‘man’ glory that is truly due to YHWH.

Yes, Yah is angry but conspiracy is real. Man is a rebellious tool of haSATAN. Our technology is being used against us.

HaSatan is a conspiratorial beast and because we are turning away from Jehovah he is being allowed to be part of the judgement.

The Bible is full of stories where God uses man or nations as tools of His judgement or blessings. King Jehu was used to rid Israel of King Ahab and Jezebel is one example.

The World Economic Forum is a conspiracy to rule the world…yah is laughing at them, but they are a tool of His judgement and because the world a large is turning away from the creator they become a tool of judgement.

In the end Yeshuah will come and save us.

The world is being Psalm 37ened.